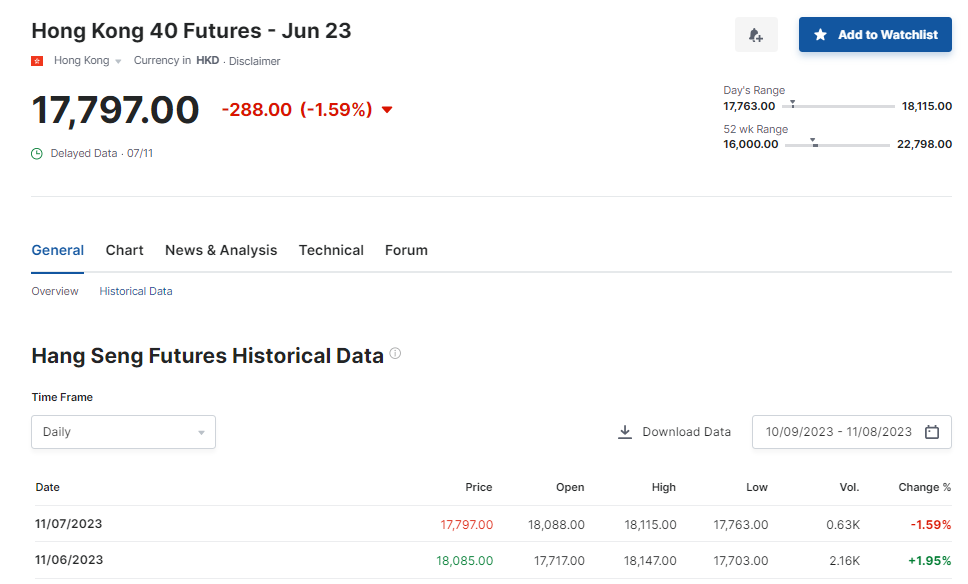

I am studying historical data of futures contract prices. I found there are price data after the settlement date of the contract. For example, for Hang Seng Futures with expiry date of Jun, there are still price data records in investing.com:

I know there could be some roll over, but isn't that being price reocord of new contracts? Why it is the case?

Also, I found for the future contract of Jun, the price data records include data for many years ago, but did the contracts start so long ago? Or is that sort of price record methods such as nearbys?