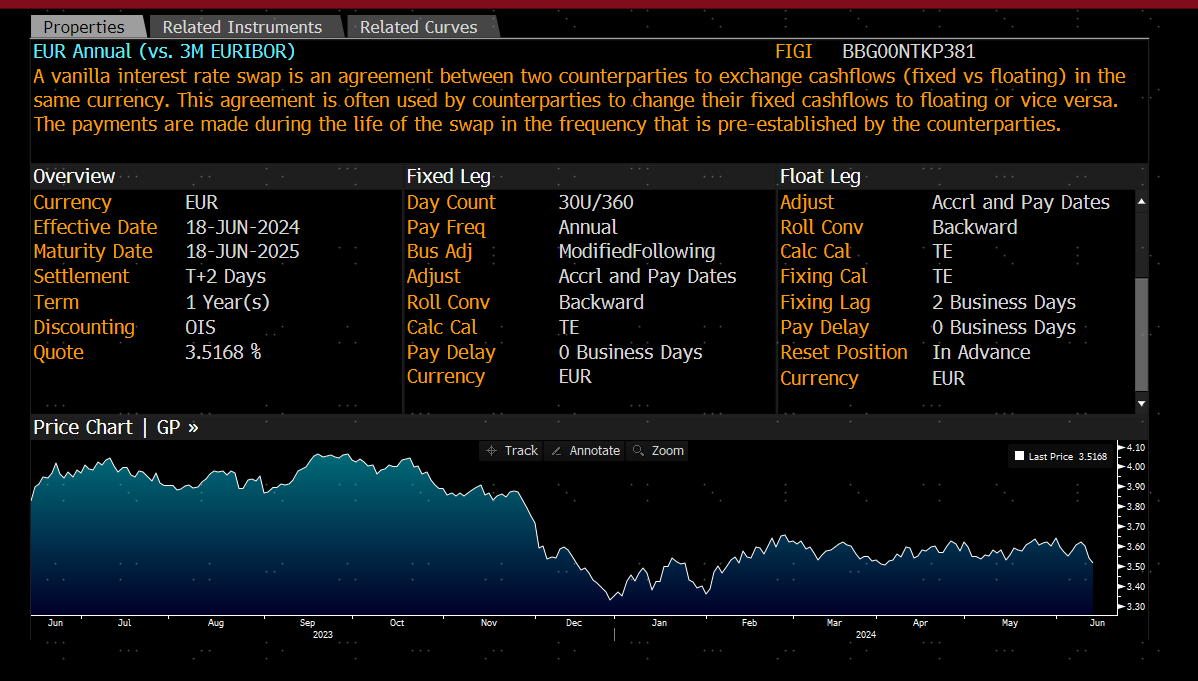

For example, EUR Annual (vs. 3M EURIBOR) swap has 2-Business-Days Fixing Lag.

When interpolating with 1Y swap, the forward 3M Euribor rate starting date is the reset date(2023/6/14), not the reset date - 2 business days(2023/6/12).

My question is does Quantlib support custom fixing lag? If anyone could answer, I'd be very grateful.