Whether you should currency hedge or not (from a mean-variance perspective) depends on the relative volatility of the asset and the currency, and on how correlated they are.

Consider an investment in a foreign-denominated asset, with a currency hedge of $w$ (where $w=0$ is unhedged, and $w=1$ is fully hedged).

If the return of the asset in local currency is $r_{\rm asset}$ and the return of a holding in the foreign currency is $r_{\rm ccy}$, then the return of this position is

$$

r_{\rm total} = r_{\rm asset} + (1 - w) r_{\rm ccy}

$$

Therefore the expected return is

$$

\mu_{\rm total} = \mu_{\rm asset} + (1 - w)\mu_{\rm ccy}

$$

and the variance is

$$

\sigma^2_{\rm total} = \sigma^2_{\rm asset} + 2(1-w)\rho\sigma_{\rm asset}\sigma_{\rm ccy} + (1 - w)^2\sigma^2_{\rm ccy}

$$

It's not unreasonable to assume that the expected return on the currency is zero, in which case you want to know what currency hedge would minimize your total variance. The hedge which minimizes the variance is

$$

w^* = 1 + \rho \frac{\sigma_{\rm asset}}{\sigma_{\rm ccy}}

$$

i.e. it depends on the ratio of volatilities of the asset and the currency, and on their correlation.

We can therefore distinguish three possible scenarios -

- The asset and currency are uncorrelated, in which case it is optimal to fully hedge the currency return.

- The asset is positively correlated with the currency (often the case for emerging market or commodity currencies) in which case it is optimal to over-hedge. Since for the typical stock you have $\sigma_{\rm asset} > \sigma_{\rm ccy}$ you may actually want to overhedge by quite a bit!

- The asset is negatively correlated with the currency (often the case for safe-haven currencies like JPY or CHF) in which case it is optimal to under-hedge, and in some extreme cases it might be optimal to not hedge at all.

The above assumes that the investor's base currency is USD. We might also consider base currencies which are not USD, e.g. an Australia-domiciled investor considering whether to hedge her exposure to a USD-denominated stock. In this case the long-run correlation between US stocks and the USD/AUD rate is about -50%, so a substantially reduced currency hedge could be appropriate.

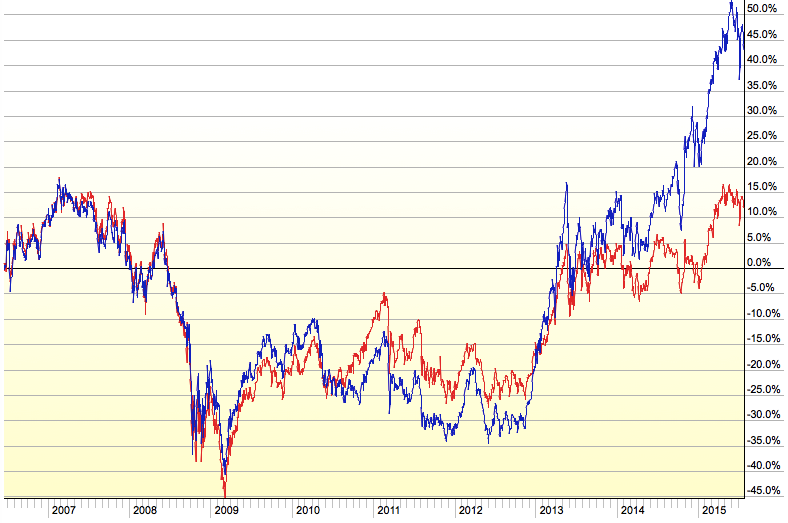

. There are clear periods where one variant is more a preferable investment over the other.

. There are clear periods where one variant is more a preferable investment over the other.