I know that a multi-period market model is complete and arbitrage free if there's a unique equivalent martingale measure. The thing is, I have absolutely no clue how to apply this theorem to a simple binomial tree. I just don't get what the two things even have to do with one another.

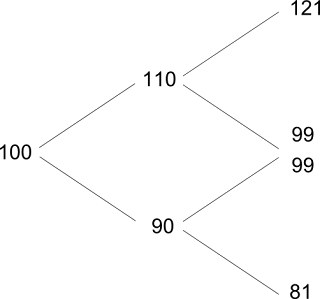

For example, consider:

Yes, I know that $u = 1.1$. I know that $d = 0.9$. But what does this have anything to do with the complicated theorem which talks about conditional expectations and equivalent martingale measures? I guess $q = (R - d)/(u-d)$ and $1 - q$ is this equivalent martingale measure but why? And why is it unique?