I'm currently reading a book which provides examples of how hedge funds employed a global macro trading strategy in the past to generate significant returns. Once such example is the convergence of European nations' government bond yields in the lead up to the launch of the Euro (monetary union).

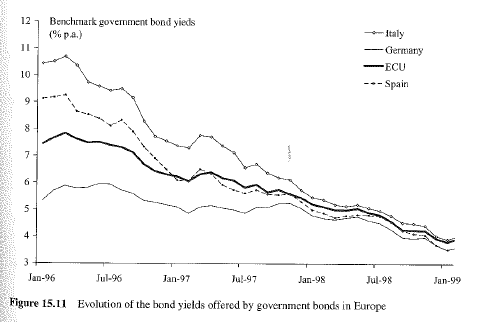

The image shows the movements of government yields in the lead up to the 99 Euro (note that pre the Euro, German debt was considered the benchmark, and all other national debt was a spread above German yields).

The book states that Hedge Funds employed a strategy of going long in Italian/Spanish debt, and going short in German debt - and that these two strategies paid off very well as convergence occurred. Furthermore, it states that the gains from such convergence trades were large because they did them via interbank currency swaps.

My question is two fold:

a) How is money made as yields decrease? Is it down to the simple fact that as yields decrease, prices increase? (Plus, why short German bonds - their yields decreased too!)

b) How did the use of currency swaps somewhat magnify the profits made? The book states that: "If the interest rate spread narrows before the contract maturity date, the investor effectively books a profit equal to the change in the spread times the number of months to maturity".

Thanks in advanced.