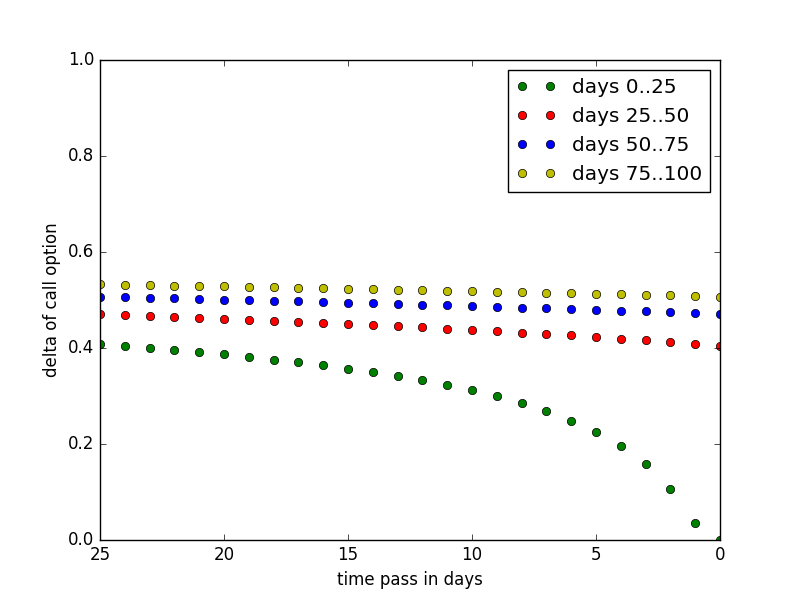

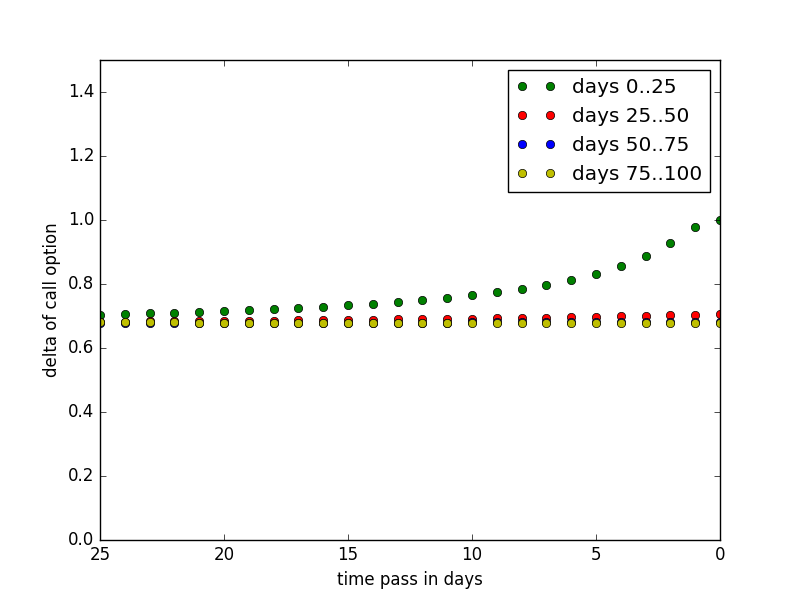

Is there any regular relationship between Delta and the Time-To-Expiry of an option?

I have observed that options that expiry sooner are more sensitive to underlying movements (with equal strikes). Is there any way to justify this relationship?

I suppose that at some point as well as the options get's closer to the expiry it's delta will be much lower for deep-in-the money or deep-out-of-the-money option.