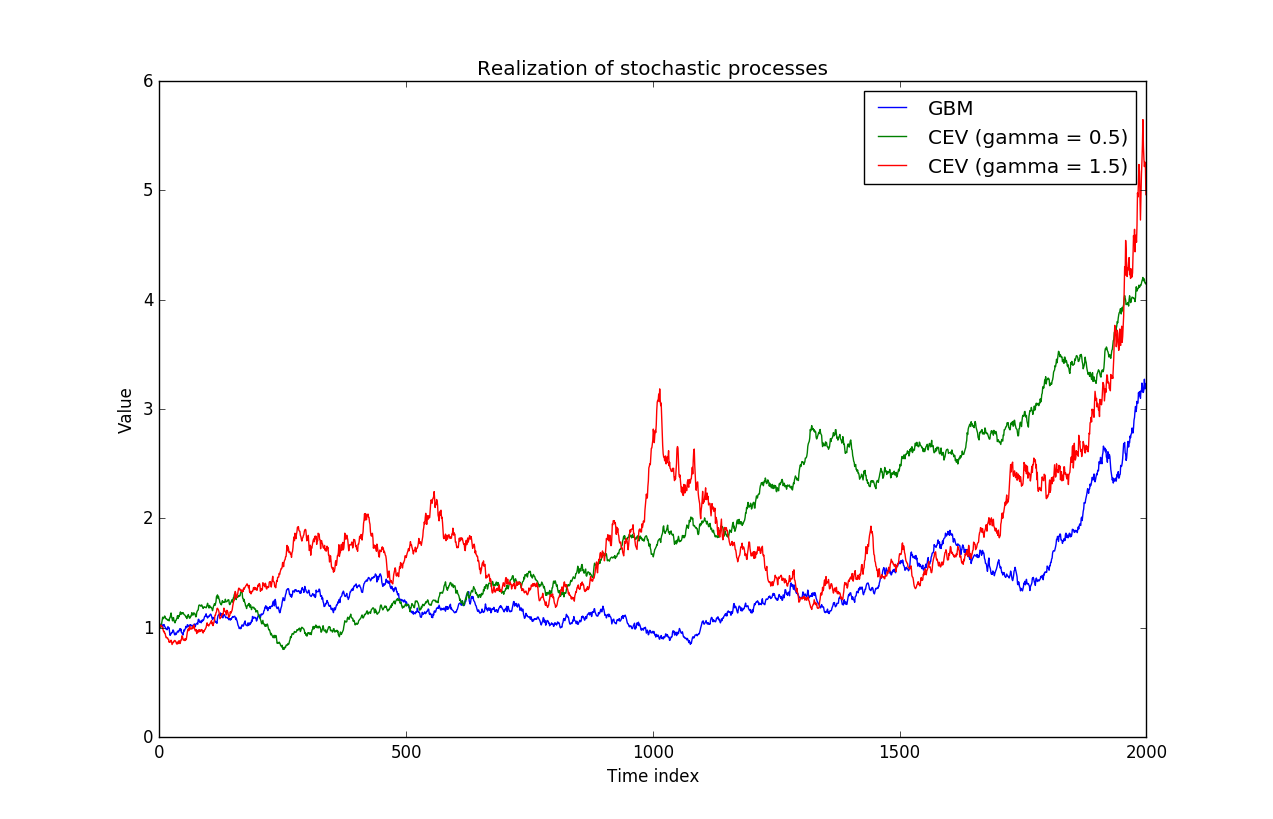

Under the CEV model the stock price has the following dynamics:

$dS_t=\mu S_tdt+\sigma S_t^\gamma dW_t$, where $\sigma\geq0, $ $\gamma\geq0$.

According to Wikipedia, if $\gamma <1$ the volatility of the stock increases as the price falls.

But why is this true? Shouldn't be the exponent negative in order to have an inverse relationship between stock price and the volatility term?