We have a stock price binomial tree model of $n$ steps, with step length $\Delta t=T/n$, stock price volatility $\sigma$ s.t. $u_n=e^{\sigma\Delta t}$ and $d_n=1/u_n$, and the risk neutral probability for each "up" movement is $p_n=(e^{r\Delta t}-d_n)/(u_n-d_n)$. It is claimed that with increasing $n$, the stock price process will in some sense approach a geometric brownian motion. The most important bridge between this discrete time model and the continuous time stochastic process is the following claim:

Let $U_n$ be the total number of "up"s throughout the whole period $[0,T]$, then clearly $U_n\sim B(n,p_n)$ (Bernoulli). By CLT we have that $$\frac{U_n-np_n}{\sqrt{np_n(1-p_n)}}\xrightarrow{\mathrm d} N(0,1).$$

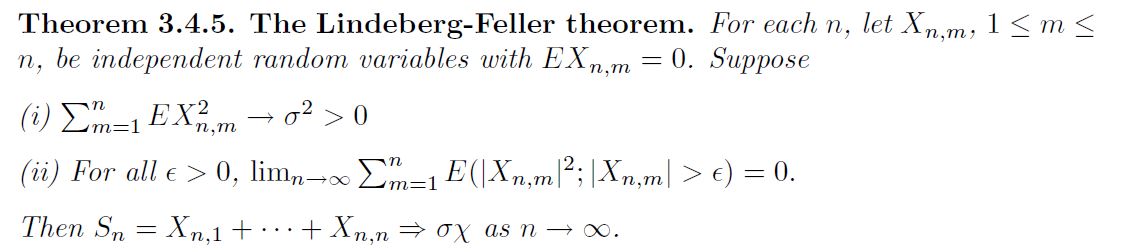

Here's how the application of CLT works as I interpret it: let $X_{1,\cdots,n}^{(n)}\sim_{\text{i.i.d.}} B(1,p_n)$, then $\Bbb EX_i^{(n)}=p_n$ and $\DeclareMathOperator{\Var}{Var}\Var(X_i^{(n)})=p_n(1-p_n)$, then pretend CLT is applicable here we should anticipate something like $$\sqrt{\frac n{\Var(X_i^{(n)})}}\left(\frac{\sum_{i=1}^nX_i^{(n)}}{n}-\Bbb E(X_i^{n})\right)\xrightarrow{\mathrm d}N(0,1).$$ Acute readers may have noticed the weird superscript $(n)$ of my $X_i^{(n)}$ here - this is also exactly where I think things go wrong: I superscript $X_i$ by $n$ because they each depend on $n$, not on $i$. In other words, when $n$ increases, the distributions of all members of the list $X_{1,\cdots,n}^{(n)}$ change simultaneously - not just the new coming ones but even the already existsing ones like $X_1^{(n)}$. This doesn't satisfy the conditions of any common version of CLT, which all require the members of the independent process depends only on its own its index but not any unspecified $n$.

Admittedly, $X_1^{(n)}$ does converge to $B(1,\frac12)$ in probability hence in distribution, since it can be shown $p_n\to\frac12$. This however is insufficient to justify applying any CLT here. So could anybody please identify which theorem (perhaps a variant of CLT) is used in proving the convergence to standard normal?