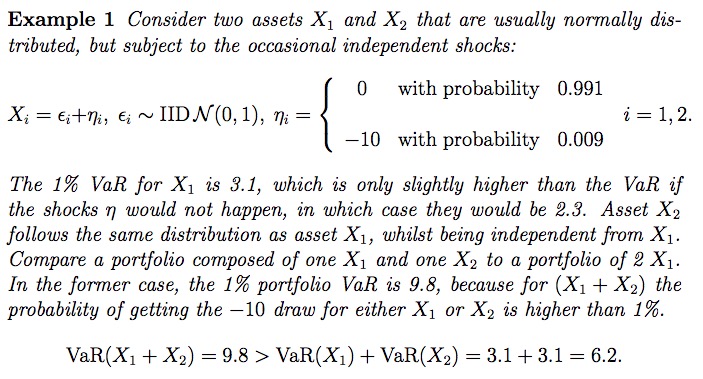

I am struggling to understand how was this simple Value-at-Risk calculated. It's Example 1 in Daníelsson, Jón, et al. "Fat tails, VaR and subadditivity." Journal of econometrics 172.2 (2013): 283-291 (a draft of which can be found in this link).

The authors consider a random variable $X_i$ defined as the sum of a standard normal random variable and a discrete random variable (which is independent from the normal r.v.).

I have attempted to obtain the distribution of $X_i$ by considering that it can be seen a mixture of gaussian distributions, with each component of the mixture representing a "regime", but I don't arrive at the same value as the authors (3.1).

I am conscious that this is a very basic exercise, but I must be missing something....

Thank you in advance for any suggestions.