Is there a standardized way of transforming the ratings of any of the major ratings agencies (S&P, Moody's, Fitch) to a numerical value. Ideally, it might be possible to create a similar scale for all of them. I just found some academic papers, which just assigned numerical values, i.e. 1 for AAA and 22 for D. Just interested if there are conventions on how to convert the ratings. Additionally, it would help comparing the impact of ratings in empirical studies.

I found some documents by ESMA, which are outlining their mappings approach.

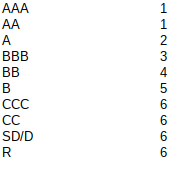

"Mapping of Standard & Poor’s Ratings Services’credit assessments under the Standardised Approach" - Link to Report In their approach the mapping is the following: