Does anyone have an explanation for the currently naturally forming volatility smile (and the variations) in the market?

$\begingroup$

$\endgroup$

4

-

$\begingroup$ The part of this question appropriate to this site is whether the assumptions of the Black-Scholes equation lead to the solution they reach. That question has been vetted by many and the conclusion is that the analysis is correct. Whether these assumptions are correct is not a mathematical question. $\endgroup$– Ross MillikanCommented Nov 9, 2012 at 4:09

-

$\begingroup$ After the 1987 crash people realized that extreme events were more likely than the log normal distribution suggests. They developed better option models, leading to the out of the money options to be priced more expensively to account for the greater risk. People still talk and think in terms of BS implied vol because 1) it is convenient, 2) many other models can be considered extensions of Black-Scholes, and 3) they can use the volatility surface from the market to price exotic options. $\endgroup$– JohnCommented Nov 9, 2012 at 4:32

-

$\begingroup$ @JoeCoderGuy, yes I think you make it a lot harder than it is. Trading volatility is not that whole lot different from trading other asset classes. The crash of 1987 simply showed market participants that the IVs far away from the money (particularly downside puts) were not fairly valued (not in terms of pricing model because the pricing model just translates IVs -> currency denominated prices but in terms of absolute level) but please see my answer for details. $\endgroup$– Matt WolfCommented Nov 12, 2012 at 2:52

-

$\begingroup$ @Gracchus, Gracchus/JoeTheCoder, when will you settle on which answer you wish to accept of your question you asked 7 months ago? You seem to change your mind every single week on numerous questions you asked. Any rational behind that? $\endgroup$– Matt WolfCommented Jun 9, 2013 at 18:11

Add a comment

|

6 Answers

$\begingroup$

$\endgroup$

1

Consider a more financially plausible model than Black-Scholes: one where the stock can suddenly go bankrupt due to fraud, and the volatility varies over time. Neither model is perfect, but the new one (call it SVJ) will be "less wrong".

Mathematically, we no longer have the Black-Scholes SDE based on a single stochastic generator $W$

$$ \frac{dS}{S} = \mu dt + \sigma dW $$

but rather an SDE with 3 generators: $W,Z$ and a jump process $J$

$$ \frac{dS}{S} = \mu dt + \sigma dW - dJ \\ d\sigma^2= \kappa(\bar{\sigma}^2-\sigma^2) dt + \eta \sigma^2 dZ $$

It is possible (though not particularly easy) to fit this more complicated, realistic model to the market. Big banks do it all the time.

Any model, including both BS and SVJ, can be run "backwards", by which I mean that it can start with an option price and derive an implied parameter. If the model has $M$ parameters $p_1, p_2, \dots, p_M$ that are normally used to find a model price $V$, then we can also choose any one of the parameters, call it $p_n$, to derive from an observed price $P$ (normally by root-finding techniques).

Let's say we run backwards from market prices to get implied values of $\sigma$ for both Black-Scholes and SVJ. You will observe a far flatter skew for the SVJ. This is true even if we remove either the jumps $J$ or stochastic volatility $Z$.

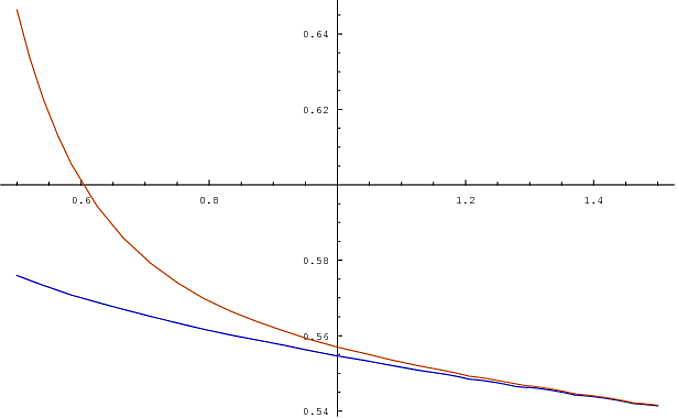

Here, for example, is a skew in Black-Scholes volatilities arising from pricing an array of options in a proprietary jump-diffusion model with flat (by strike) volatility of 20%

We see that a constant volatility parameter in the jump-diffusion is equivalent to a skew of Black-Scholes volatilities.

Conclusion: the smile comes from the model being too strong a simplification of reality.

-

2

$\begingroup$

$\endgroup$

$\endgroup$

4

Implied volatility has very little to do with any particular pricing model, especially not much with BS. BS is a translation tool between prices and volatility, with its own many model deficiencies. I won't get into such model assumptions because my point is an entirely different one. Even the smile/smirk is entirely unrelated to the Black-Scholes model and I read your question that you like to understand why IVs, far from the money, are higher than close to the money ones.

My point is that IVs are entirely supply and demand driven. Whether its the IVs of an option that expires a year from now or tomorrow, whether its the IV of a 90 put (equity option), 30 delta strike (fx), or any other rates option, commodity option, what have you...

Someone correctly pointed out that most of the origin of the smile/smirk can be traced back to the October 1987 shock ( http://en.wikipedia.org/wiki/Black_Monday_(1987) )

Before pretty much all IVs regardless of moneyness were priced equally. However, the market after the stock market crash found that primarily downside protection was priced way too cheaply. Now I guess the core of the question is why: Most can be attributed to those who generally wrote such options such as sell-side trading desks but especially also floor traders who made markets in such options. They suffered steep losses and found out that they were not enough compensated for writing options such deep out of the money. It has to do with the fact that the market under-estimated the probability of such extreme events happening.

However, another important finding that causes many market makers to trade IVs far away from the money higher than at the money ones has to do with the belief that return volatility far away from current price levels tends to be a lot higher than current return volatility. For example, return volatility is expected to be higher at 20% lower market levels than current return volatility. I guess the rational behind that is in a sense a paradox: Nobody generally would need to care about an instantaneous move 10% or so lower from current levels, thus in a sense it does not matter which implied volatilies are attached to a 90 put. However, should the unexpected happen than the expectation is for sharply higher return volatility 10% below current levels. Keep in mind the smile/smirk is dynamic and only reflects current expectations. I have seen on numerous occasions "inverted smirks" in equity index and stock options in that out of the money calls exhibited higher IVs than out of the money puts. But generally in this asset class space out of the money puts exhibit higher IVs than equally spaced out of the money calls.

Another point that supports this general shape of the "smirk" is that empirically stock markets exhibit much higher down-side return volatility than up-side return volatility. Panic and fear in a sense causes more irrational behavior in people than exuberance.

So, in summary, all has to do with how the market prices the probability of shocks (to the down and upside) occurring and their severity.

EDIT: Please keep in mind that most all IVs away from current spot/forward levels exhibit the property of being more richly priced than ATM IVs. On the call side this is the case because nowadays options are often utilized as leveraged bets instead of buying the underlying outright. Put IVs that are struck below current spots/forwards are bought more aggressively because of the desire to protect long positions in the underlying (buy-side fund industry especially). IVs away from the money are simply more demanded than ATM ones because of the above reasons. I recommend you do not read a whole lot more into it than this because trading volatility in the end of the day is nothing else than trading any other asset, prices are set as a pure function of supply and demand, the only difference is that most underlying assets exhibit linear pay off functions where as volatility is non-linear in nature and market participants can exactly define how this non-linearity is structured by trading different strikes or option combinations.

Research suggests that there is a relationship between how pronounced the smirk is and future return expectations in the underlying. This hardly surprises me because in a sense it reinforces what I explained above in that people either protect with down side puts if they expect the underlying to exhibit future negative returns and equally buy upside calls (often as a leveraged bet instead of the underlying) if they expect future returns in the underlying to be positive, hence the smile = higher IVs away from the money.

answered Nov 10, 2012 at 12:11

-

$\begingroup$ I have to disagree that down-side return volatility is much higher than up-side return volatility---historical returns are in fact negatively skewed, but only slightly. If you look at actual data, you will find many extreme upside moves to balance the downside. $\endgroup$– justin--Commented Nov 10, 2012 at 17:52

-

1$\begingroup$ @Freddy do you agree that IV are computed using market prices and some formula $f(...,\sigma)=p$? $\endgroup$– SRKXCommented Nov 10, 2012 at 18:43

-

2$\begingroup$ @justin, feel free to run your own analysis over a time series that comprises a longer period of time. You find that realized vol was the highest when markets crashed and not when market topped out (on average). This is pretty much an established fact and you can feel free to google numerous academic papers that investigated this. $\endgroup$ Commented Nov 11, 2012 at 1:39

-

3$\begingroup$ @SRKX, absolutely disagree, and I disagreed in my comment to your answer already. Implied vols are not the outcome of any pricing model, implied vols are a market consensus and, for example, the BS model is a mere translation tool from implied vols -> currency denominated prices. Listed options prices are not a result of supply and demand of an option but supply and demand for implied volatility. If you insist IVs are the result of some formula then I highly doubt you ever worked as volatility trader. $\endgroup$ Commented Nov 11, 2012 at 1:43

$\begingroup$

$\endgroup$

3

The Black-Scholes model is based on the assumption of lognormal returns of the underlying asset. There is much evidence and argument that stock market returns are not normal on a logarithmic basis, and there is no particular reason to assume a normal distribution, either. In particular an implied volatility smile is evidence of "fat tails" in the returns expected by market participants---excess kurtosis, if you will. It's been pointed out by Taleb that with over 100 years of history, we simply don't have enough data to estimate the tails or the higher moments of the distribution of stock market returns.

Edit: in R:

> library("moments")

> SPX <- read.csv("http://ichart.finance.yahoo.com/table.csv?s=%5EGSPC&d=10&e=10&f=2012&g=d&a=10&b=10&c=1992&ignore=.csv")

> kurtosis(diff(log(SPX$Adj.Close)))

[1] 11.36604

That's for the last twenty years less a day of data, and does not include the crash of 1987. For a normal distribution, we would expect the kurtosis to be 3. The excess kurtosis in this case is $11.36604-3=8.36604$, which is still quite significantly not normal. Excess kurtosis means that a distribution has a more peaked center and fatter tails than a normal distribution, which means in the case of options a higher probability that the underlying will take on values far away from its current value come expiration time. This is why, when excess kurtosis is not taken into account, options further from the money appear to imply a higher volatility for the underlying asset.

-

1$\begingroup$ Just did what you said --- I was curious myself --- the returns are quite leptokurtic, not normal. $\endgroup$– justin--Commented Nov 10, 2012 at 1:05

-

$\begingroup$ The double-sided exponential distribution happens to be the fattest-tailed distribution that has a moment-generating function---but just barely---its mgf has vertical asymptotes which may impair one's ability to derive an equivalent martingale distribution (of the same exponential family) suitable for pricing options as in the Black-Scholes model. $\endgroup$– justin--Commented Nov 10, 2012 at 1:40

-

1$\begingroup$ @JoeCoderGuy You might want to check this article out: Shalom Benaim and Peter Friz. Smile Asymptotics II: Models with Known Moment Generating Functions. Journal of Applied Probability , Vol. 45, No. 1 (Mar., 2008), pp. 16-32 $\endgroup$– justin--Commented Nov 13, 2012 at 5:49

$\begingroup$

$\endgroup$

5

The volatility smile is made out of implied volatilities. This means that you take as input $K,S,r,T$ and the price of the option $p$ and you use it to find $\sigma$ such that

$$ p = BS(K,S,r,T,\sigma)$$

But $p$ is defined by the market, so the $\sigma$ you find are the estimated volatilities by market participants, if they believe in the Black Scholes framework.

The shape of the graph (a smile) shows that, in the BS framework, market participants estimate different volatilities for a same asset depending on the moneyness of the option. This means that the BS framework does not hold in reality (at least market participants don't believe in it), as for the same asset, it assumes that $\sigma$ is constant.

-

$\begingroup$ I don't think it's only missing a variable, there are various weak points to the theory (normality of returns for example). Your question was about interpreting implied volatilities, and I'm answering that IV can't really be interpreted because they rely on a "wrong" model yielding contradictory results. $\endgroup$– SRKXCommented Nov 10, 2012 at 11:11

-

$\begingroup$ I am not sure I agree with you saying "IV can't really be interpreted because they rely on a "wrong" model...". IV are not underlying any model at all. IVs across the smile is how market consensus prices risk. I has nothing to do with any model in a very similar way than absolute stock prices have everything to do with market consensus and very little to do with any pricing model. Please see my answer for what I mean with that in more detail. $\endgroup$ Commented Nov 10, 2012 at 11:22

-

2$\begingroup$ @Freddy you compute IV using the BS formula.... if that's not assuming a model then I don't know what it is. It means "what would be the volatility taken by market participants if they used the BS formula to price their option?". Well that's pretty much depending on BS to me. $\endgroup$– SRKXCommented Nov 10, 2012 at 12:00

-

$\begingroup$ @SRKX, sorry but I strongly disagree. Pretty much all direct market participants who manage risk on the volatility side trade volatility not options prices. The translated prices are an agreed faulty way of paying for the bought or sold volatility. The asset that is traded and priced is volatility. Nobody cares about BS when considering whether to take risk in buying or selling an option, BS comes into play when looking to calculate the price that is paid/received for the volatility that is traded. $\endgroup$ Commented Nov 10, 2012 at 12:14

-

$\begingroup$ just in case the following causes confusion: I did not want to say "IV are not underlying any model at all" but wanted to say "IV are not relying on any model at all". Sorry for the confusion but I could not edit the original comment anymore $\endgroup$ Commented Nov 10, 2012 at 12:23

$\begingroup$

$\endgroup$

0

I agree with some arguments above.

One can find several explanattion to volatility smile:

Against the BS framework assumption, volatility is not constant and traders don't expect it to be constant

This is a matter of option supply and demand

volatility smile incorporates the kurtosis seen in the underlying

One can find hints on this issue in P.Wilmott's Frequently asked question in quantitative finance

$\begingroup$

$\endgroup$

The Black-Scholes model was based on assuming lognormal stock price fluctuations with a constant volatility. However, the modern practice is to use the Black-Scholes formula not as a prediction but merely as a parametrization of option prices, where the observed price of a given option at a given time translates to a "local" implied volatility (IV). Thus, when the resulting IV varies over strikes and over time, it is parametrizing a breakdown of the original Black-Scholes assumptions. Predicting an option price is tautologically reframed as predicting the corresponding IV. At most we can say that if the original Black-Scholes assumptions are roughly right, the IV is roughly constant.

The volatility smile is an expected result of stock price fluctuations with heavier tails than lognormal. That is, sudden very large moves up or down due to news or sentiment shifts, though rare, are less rare than the lognormal distribution indicates. (See the work of Nassim Taleb.) In the absence of a replacement for Black-Scholes that actually models the more accurate distribution, we patch it up by noting that the further out-of-the-money options are priced as if the underlying lognormal volatility were higher (a proxy for the heavier tails).