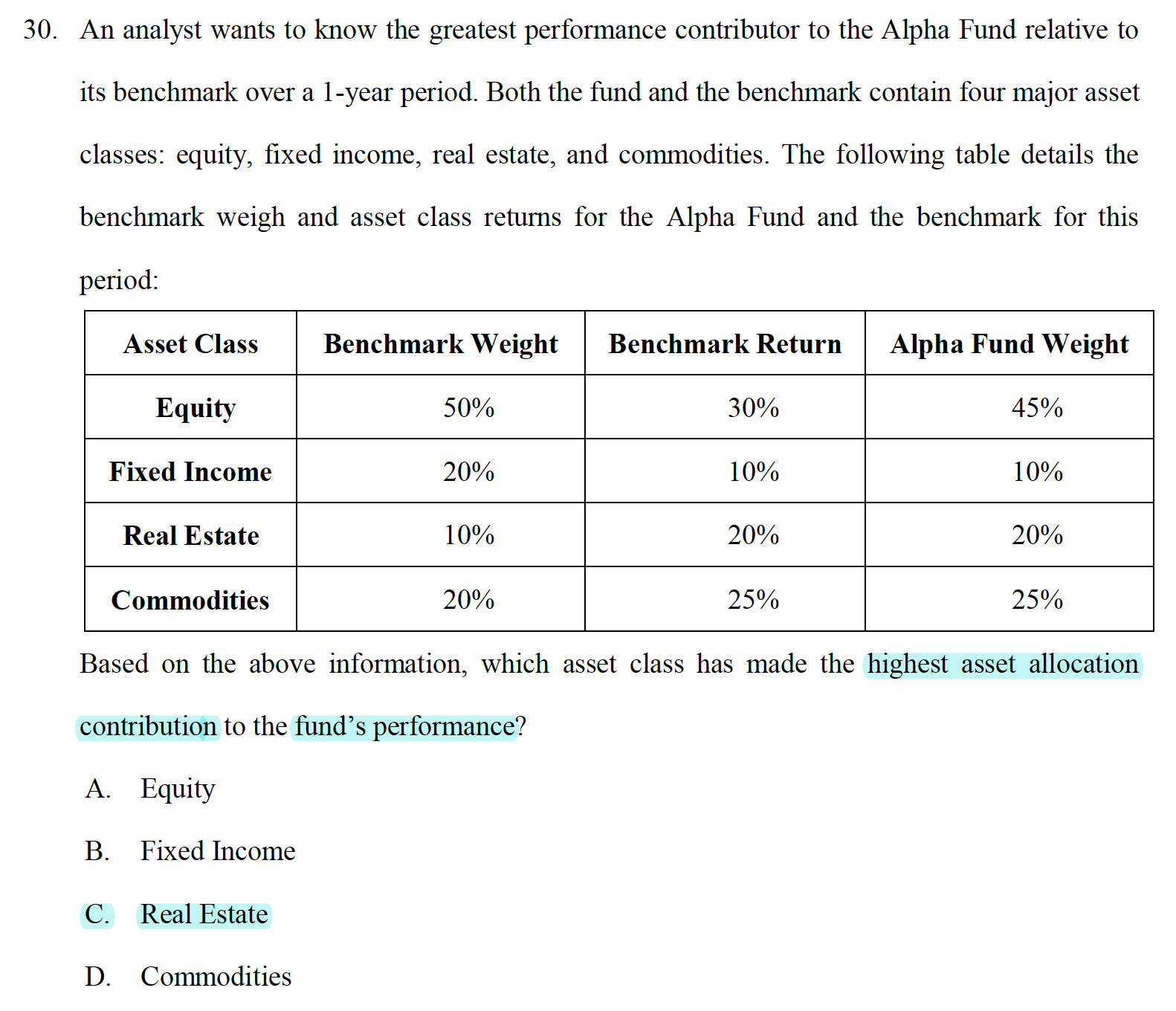

Comparing the contributions using Fund Weights versus using Benchmark weights:

Sect ret fundw contrib ret bweigt contrib difference

A 0.3 0.45 0.135 0.3 0.5 0.15 -0.015

B 0.1 0.1 0.01 0.1 0.2 0.02 -0.01

C 0.2 0.2 0.04 0.2 0.1 0.02 0.02

D 0.25 0.25 0.0625 0.25 0.2 0.05 0.0125

Total 0.2475 0.24 0.0075

Conclusion: the fund's chosen asset allocation outperformed the benchmark by 75 bps (return of 24.75% versus benchmark return 24%), this was mostly due to Sector C (Real Estate) which had a generous overallocation (20% instead of 10%) and satisfactory (but not top) returns (20%) resulting in an 0.02 difference (last column). Sector D also contributed to outperformance, but to a lesser degree (0.0125).