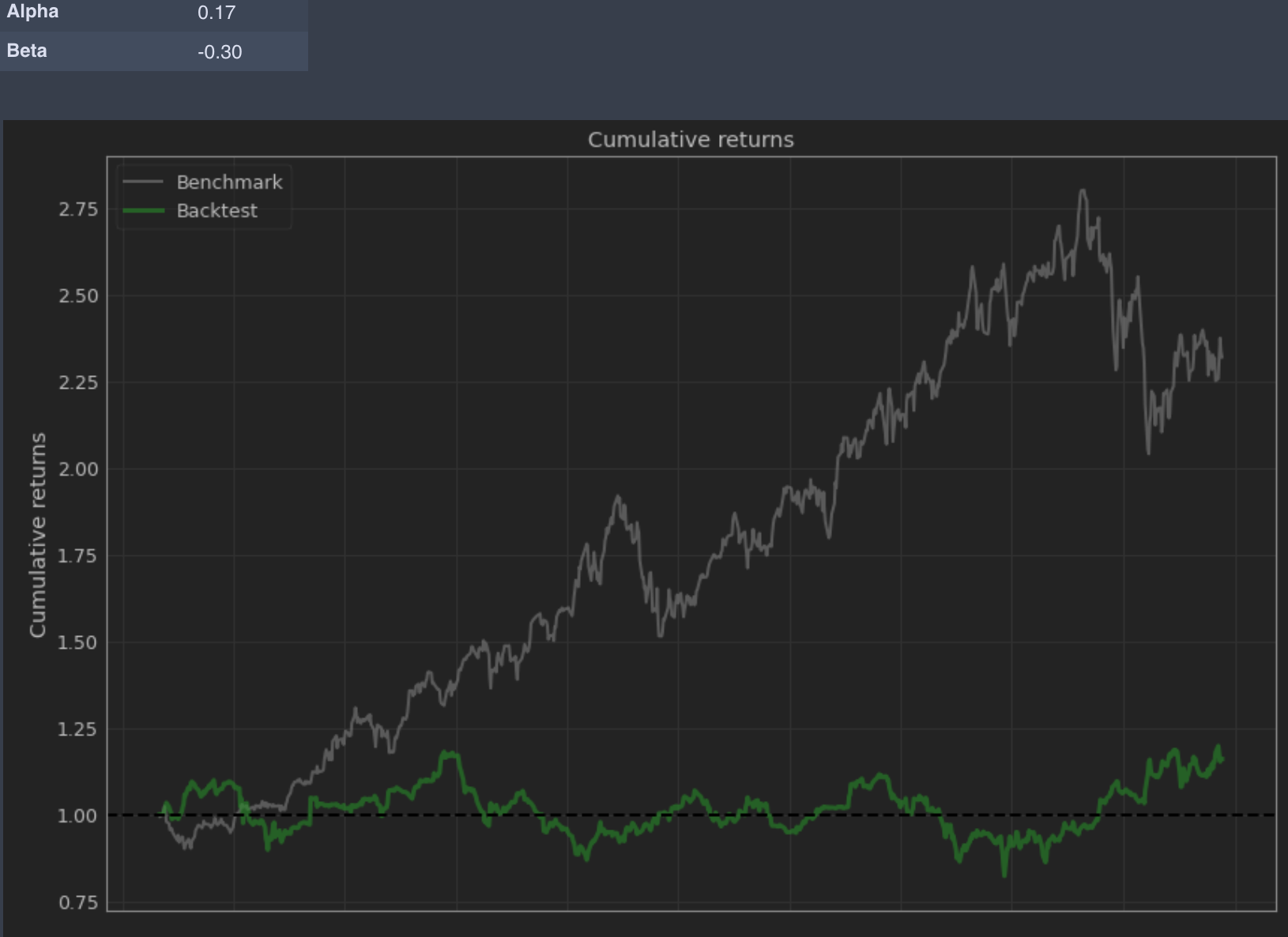

According to my portfolio analysis program (pyfolio), the alpha of the following strategy is .17 (I am assuming 17%). [Based on pyfolio documentation, alpha here is the "annualized alpha".]

However, the cumulative returns of the benchmark are about 10-fold higher than that of the strategy (~12% vs ~125%), see graph.

To me this is non-intuitive, and I was wondering if someone had a good explanation.

Does beta (negative in this case) have something to do with it?

Of course, it is also possible that I am not using the software correctly, or misinterpreting its output. I will go into its source code to try and figure out the calculation it performs. But I hoped someone knows what might be going on here. Thanks!

UPDATE: Here's a link to a csv file with returns: https://drive.google.com/file/d/1m04SfUPzYdB9fPPSLMHbNq5iM0LWf3fc/view?usp=sharing