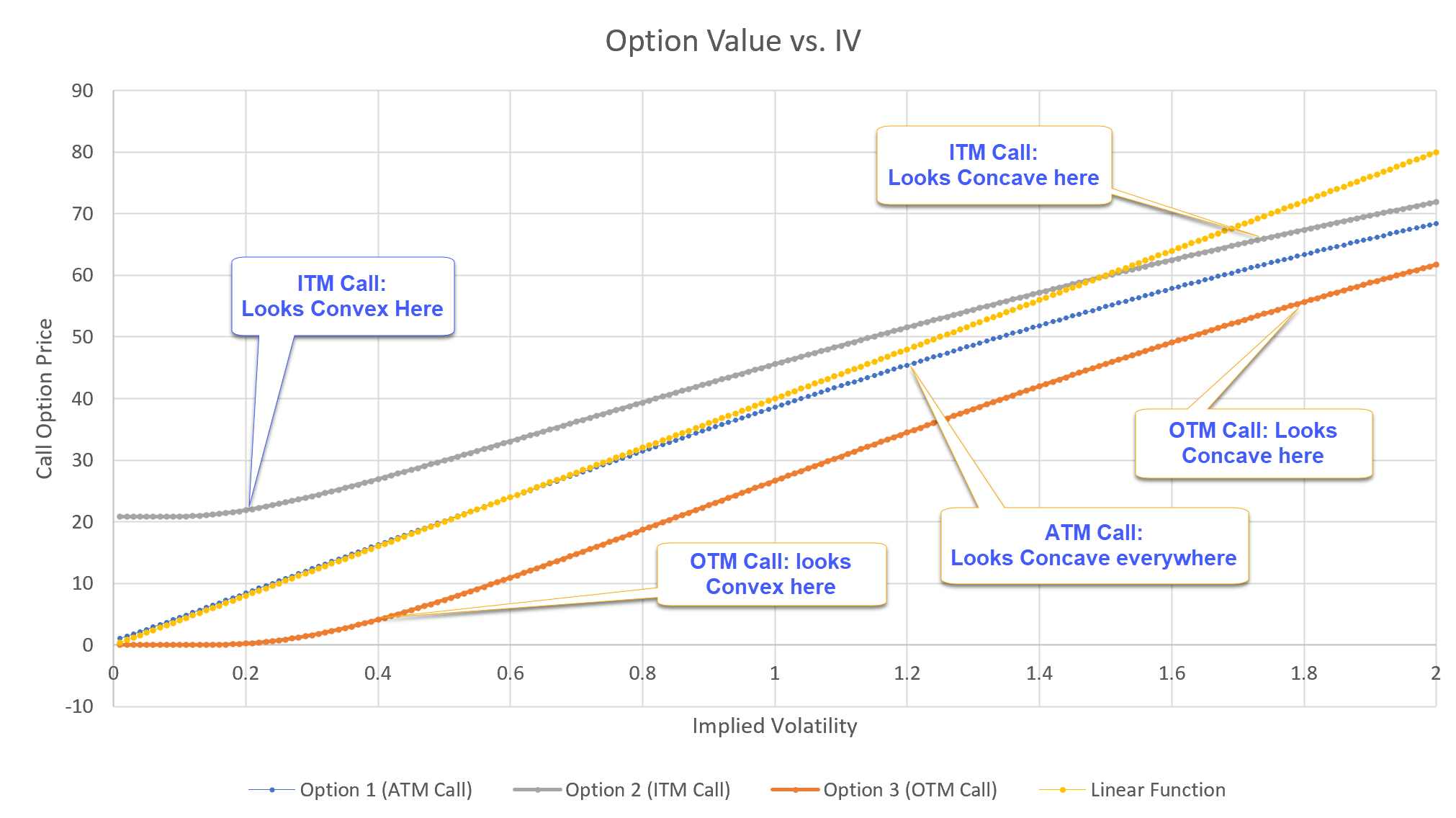

I was doing an exercise on investigating the relationship between European Call option price and its volatility. I was asked to compute $\frac{\partial^2C}{\partial \sigma^2}$ and find out the domain of $\sigma$ on which the option price $C$ is convex.

I got the second order derivative as shown: $$ \frac{\partial^2C}{\partial \sigma^2} = Vega \cdot \frac{d_1d_2}{\sigma}, $$ where $d_1, d_2$ are the parameters in Black Scholes formula. To find the required domain, I let the second order derivative to be non-negative, and I argue that $Vega$ is always non-negative, so I need $d_1$ and $d_2$ with same sign.

I am not sure if my approach is correct or not, since I got a quite wierd range for $\sigma$: $$ \sigma \le \sqrt{\frac{2(\log S_t/K + r(T-t))}{T-t}}, $$ or $$ \sigma \le \sqrt{\frac{2(-\log S_t/K - r(T-t))}{T-t}}. $$