Could anyone please give the detailed expression of either the close-close or open-close volatility ?

Thanks

Could anyone please give the detailed expression of either the close-close or open-close volatility ?

Thanks

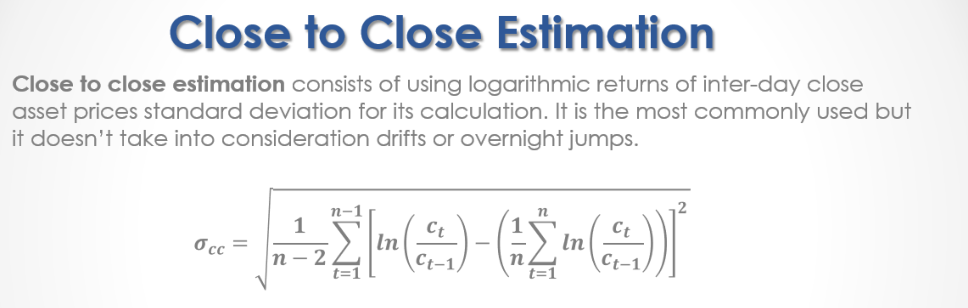

Standard deviation method Historical price returns also on close prices

stdev = historical = sqrt[(x- (sum x/n))^2]

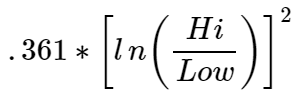

The simplest method for Parkinson's High Close method is

The high Low method is statistically more efficient than the standard close method. However it assumes continuous trading and observations of high and Low prices. The method can therefore underestimate the true volativity.

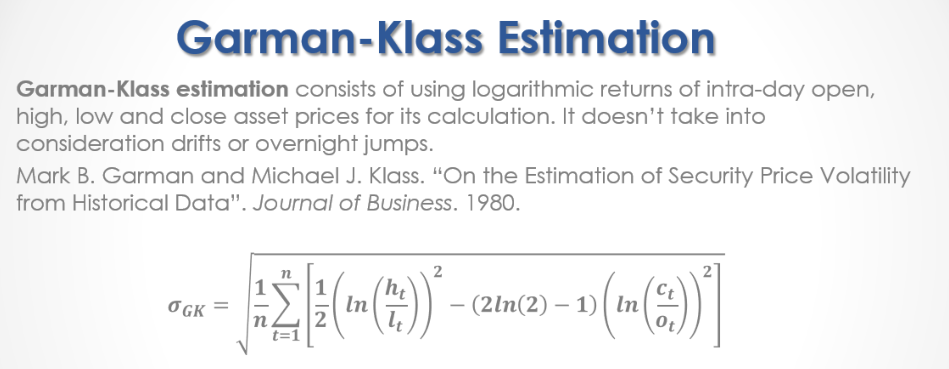

The Garman Klass High Low Close Method, can once again underestimate volatity