Variance Premia; disentangled.

Let me address this question a bit differently and bring the question forward: What part (i.e. 'side') of the volatility smile attracts a significant premium in relationship to the underlying uncertainty that it is trading?

To this end, let us define the physical, i.e. empirical (average realized) return semivariance as:

$$

SV_\mathbb{P}^-=\mathbf{E}^\mathbb{P}\left((r-\mu_\mathbb{P})^2\mathbf{1}_{\{Z\leq\mu_\mathbb{P}\}}\right)=\int_{-\infty}^{\mu_\mathbb{P}}(z-\mu_\mathbb{P})^2p(r)dr

$$

and define its risk neutral, i.e. option implied, equivalent $SV_\mathbb{Q}^-$ in the same manner. Do the same for the empirical, and priced, upside semivariances likewise. We can now define a downside (and upside) semivariance risk premium as the:

$$

\begin{align}

DSP(r)&\equiv SV_\mathbb{P}^-(r)-SV_\mathbb{Q}^-(r)\\

USP(r)&\equiv SV_\mathbb{P}^+(r)-SV_\mathbb{Q}^+(r)\\

\end{align}

$$

In a nutshell: DSP is the average realized profit (ex trading cost) from buying downside semivariance options in the market; USP is the average realized profit from buying upside semivariance options in the market. A portfolio of both, upside and downside, replicates a VIX position (more or less).

We can now re-use the VIX development and arrive at a put/call based pricing formula for the downside (or upside) priced semivariance:

$$

SV_\mathbb{Q}^-=\mathrm{E}^\mathbb{Q}\left({\left(\log\left(\frac{S_T}{S_0}\right)-\mu_\mathbb{Q}\right)^21_{\left\{\log\left(\frac{S_T}{S_0}\right)\leq \mu_\mathbb{Q}\right\}}}\right)=\int_0^{S_0e^{\mu_\mathbb{Q}}}\frac{1-\log\left(\frac{X}{S_0e^{\mu_\mathbb{Q}}}\right)}{\frac{1}{2}B_0(T)X^2}Put(X)\mathrm{d}X

$$

with $X$ the option strike, $\mu_\mathbb{Q}$ the risk neutral drift, $S_0$ today's index level and and $S_T$ the index level at expiry. We finally define some measure for the empirically observed semivariance and are in a position to test the premia, i.e. ask the question:

Is the Downside (upside) semivariance premium significant?

Source: https://www.sciencedirect.com/science/article/abs/pii/S0378426620301412

Source: https://www.sciencedirect.com/science/article/abs/pii/S0378426620301412

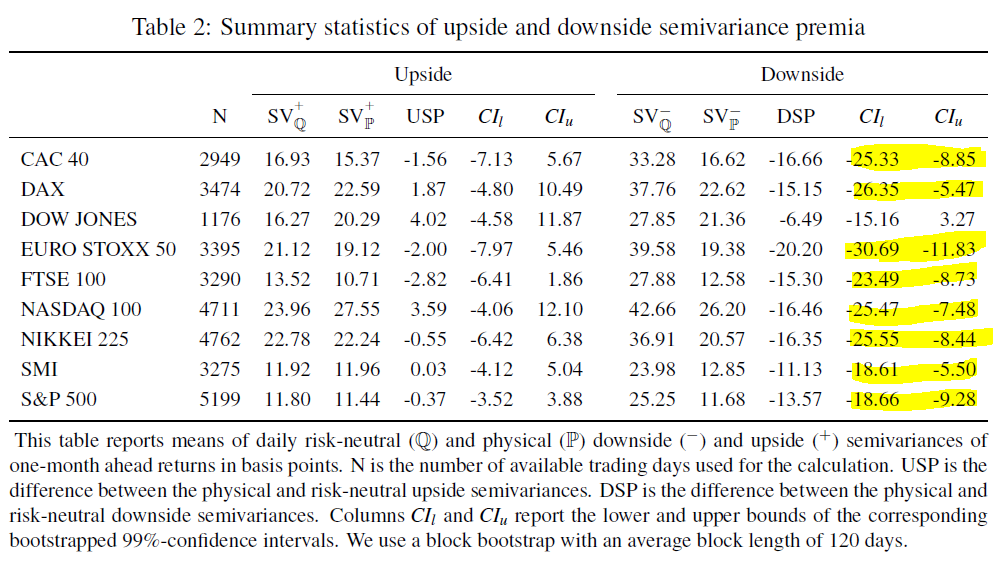

For major stock market indices, we find quite similar results (see below): Whereas the upside semivariance premium is often quite small and not statistically significant (99% confidence interval around zero), the downside semivariance premium is economically and statistically significant. Hence:

there is a general pattern in investor behavior to insure against large return innovations in the negative but not in the positive return domain.

and even more so:

the major part of the variance premium is paid to insure against extreme negative return realizations. For a return horizon of 30 days, the variance premium for returns below -15% amounts to values of around -15 bp for all considered indices.

HTH a bit?

NB: ... It would be an interesting endeavor, of course, to replicate this analysis using stocks and stock options.