I'm using Quantlib in Python to price an FX option. I'm comparing the result to Bloomberg, to make sure the code is working correct.

I want to calculate the P&L of a certain option trading strategy by using Taylor expansion of P&L (discussed in other post here) And also by using the NPV of the option.

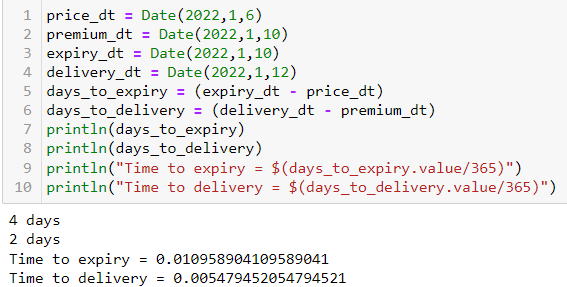

Therefore, it's important to have a correct NPV for every date that the option is alive. The option I use to test this is a 1-week stylized option.

The problem that occurs is that the NPV matches Bloomberg correctly on the first, second, third and last date, but not on the other dates.

import QuantLib as ql

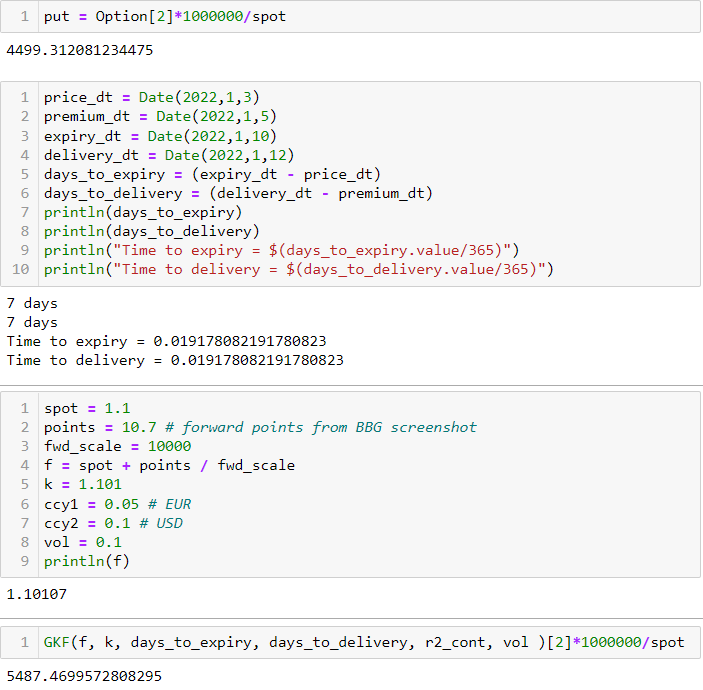

Spot = 1.1

Strike = 1.101

Sigma = 10/100

Ccy1Rate = 5/100

Ccy2Rate = 10/100

OptionType = ql.Option.Call

#Option dates in quantlib objects

EvaluationDate = ql.Date(3, 1,2022)

SettlementDate = ql.Date(5, 1, 2022) #Evaluation +2

ExpiryDate = ql.Date(10, 1, 2022) #Evaluation + term which is 1 week

DeliveryDate = ql.Date(12, 1, 2022) #Expiry +2

NumberOfDaysBetween = ExpiryDate - EvaluationDate

#print(NumberOfDaysBetween)

#Generate continuous interest rates

EurRate = Ccy1Rate

UsdRate = Ccy2Rate

#Create QuoteHandle objects. Easily to adapt later on.

#You can only access SimpleQuote objects. When you use setvalue, you can change it.

#These global variables will then be used in pricing the option.

#Everything will be adaptable except for the strike.

SpotGlobal = ql.SimpleQuote(Spot)

SpotHandle = ql.QuoteHandle(SpotGlobal)

VolGlobal = ql.SimpleQuote(Sigma)

VolHandle = ql.QuoteHandle(VolGlobal)

UsdRateGlobal = ql.SimpleQuote(UsdRate)

UsdRateHandle = ql.QuoteHandle(UsdRateGlobal)

EurRateGlobal = ql.SimpleQuote(EurRate)

EurRateHandle = ql.QuoteHandle(EurRateGlobal)

#Settings such as calendar, evaluationdate; daycount

Calendar = ql.UnitedStates()

ql.Settings.instance().evaluationDate = EvaluationDate

DayCountRate = ql.Actual360()

DayCountVolatility = ql.ActualActual()

#Create rate curves, vol surface and GK process

RiskFreeRateEUR = ql.YieldTermStructureHandle(ql.FlatForward(0, Calendar, EurRateHandle, DayCountRate))

RiskFreeRateUSD = ql.YieldTermStructureHandle(ql.FlatForward(0, Calendar, UsdRate, DayCountRate))

Volatility = ql.BlackVolTermStructureHandle(ql.BlackConstantVol(0, Calendar, VolHandle, DayCountVolatility))

GKProcess = ql.GarmanKohlagenProcess(SpotHandle, RiskFreeRateEUR, RiskFreeRateUSD, Volatility)

#Generate option

Payoff = ql.PlainVanillaPayoff(OptionType, Strike)

Exercise = ql.EuropeanExercise(ExpiryDate)

Option = ql.VanillaOption(Payoff, Exercise)

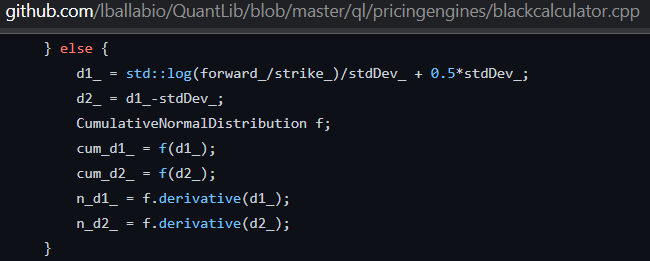

Option.setPricingEngine(ql.AnalyticEuropeanEngine(GKProcess))

BsPrice = Option.NPV()

ql.Settings.instance().includeReferenceDateEvents = True

ql.Settings.instance().evaluationDate = EvaluationDate

print("Premium is:", Option.NPV()*1000000/Spot)

ql.Settings.instance().evaluationDate = EvaluationDate+1

print("Premium is:", Option.NPV()*1000000/Spot)

ql.Settings.instance().evaluationDate = EvaluationDate+2

print("Premium is:", Option.NPV()*1000000/Spot)

ql.Settings.instance().evaluationDate = EvaluationDate+3

print("Premium is:", Option.NPV()*1000000/Spot)

ql.Settings.instance().evaluationDate = EvaluationDate+4

print("Premium is:", Option.NPV()*1000000/Spot)

ql.Settings.instance().evaluationDate = EvaluationDate+7

print("Premium is:", Option.NPV()*1000000/Spot)

Which results in:

Premium is: 5487.479999102207

Premium is: 5148.552323458257

Premium is: 4774.333578225227

Premium is: 4353.586300232529

Premium is: 3867.4561591587326

Premium is: 909.0909090908089

However, according to Bloomberg the premium should be:

5487.48 (correct)

5148.55 (correct)

4774.33 (correct)

4499.5

4015.7

909.9 (correct)

The result on expiration is given by setting the following (the option expires in-the-money):

ql.Settings.instance().includeReferenceDateEvents = True

Can someone explain why the NPV suddenly doesn't match for those 2 dates?

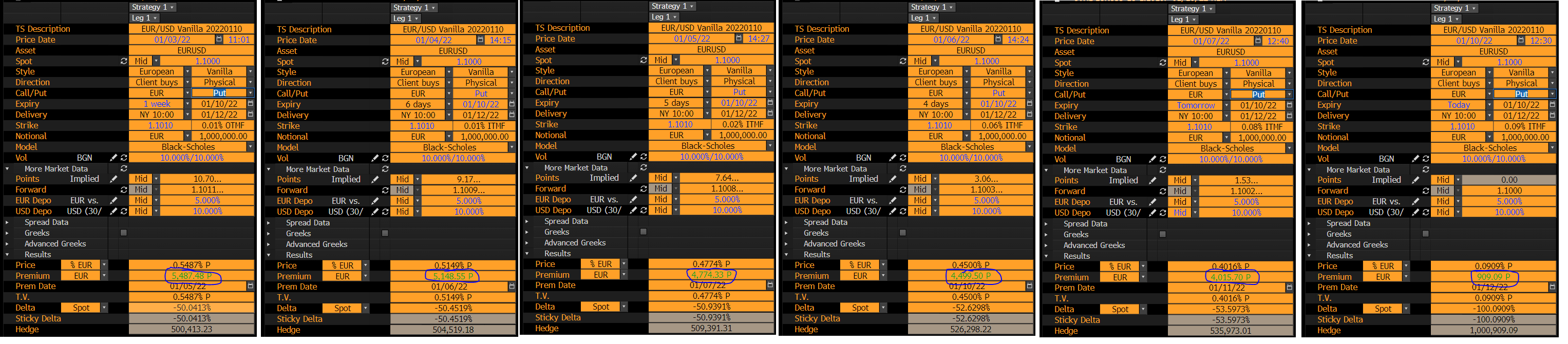

Screenshots of option pricing in Bloomberg