When trying to value an American option we often use grid-based methods (e.g. Monte Carlo in combination with Longstaff Schwartz; or Finite Difference Methods). As such, we are in fact estimating the value of a Bermudan option with discrete time points where we can exercise the option, i.e. $0=t_0 < t_1 < ... < t_n = T$.

However, as the time grid gets finer the value of the Bermudan option converges to the American option. I have heard that the rate of convergence is of order $O(\Delta t)$. How can this be shown analytically?

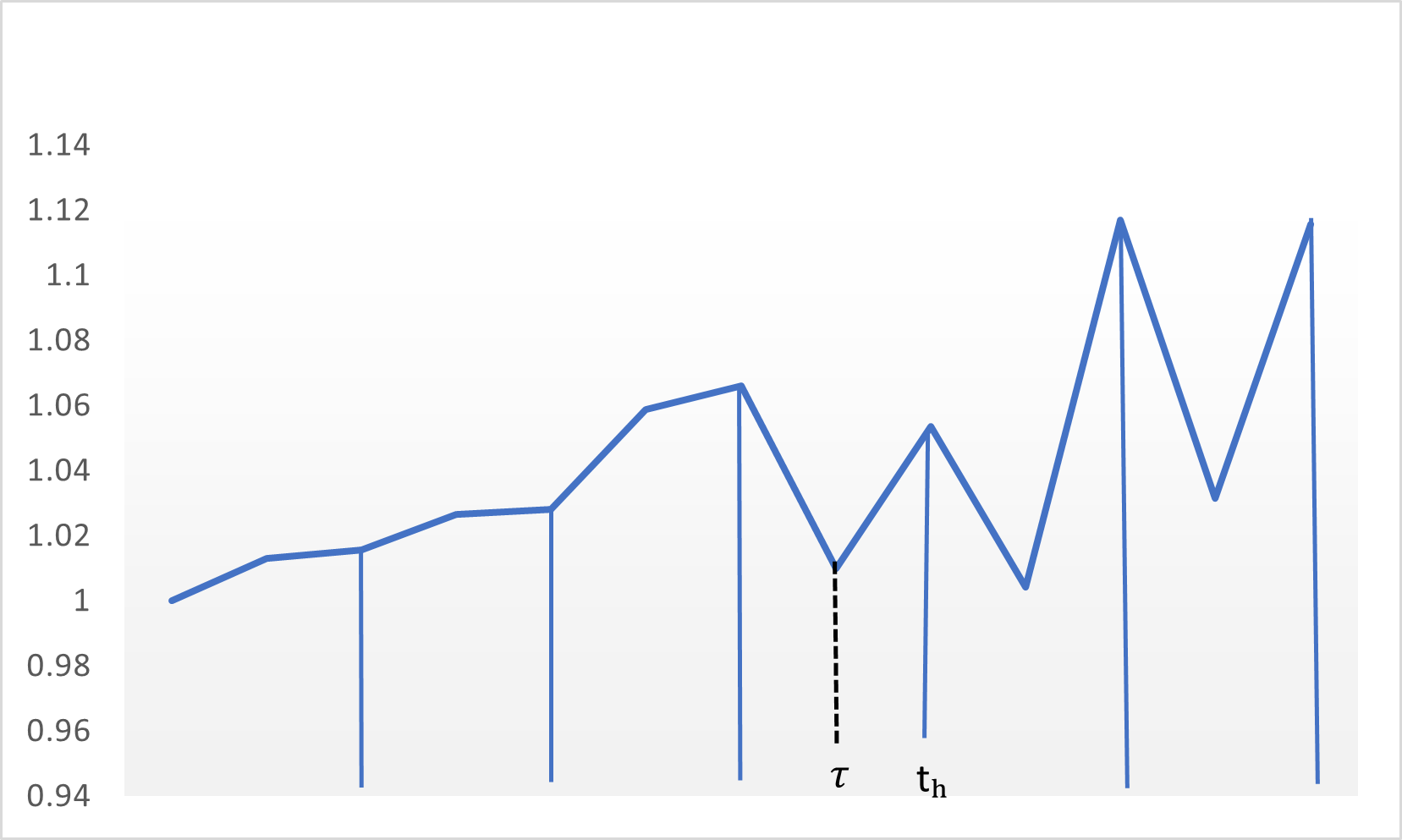

I am especially considering the following exercise strategy

- Find the optimal exercise time of the American option, $\tau^*$, where $t_{h-1}<\tau^* < t_{h}$,

- Exercise the Bermudan option at the first time point after $\tau^*$, i.e. at time $t_{h}$.

My starting point would be to have a look at the price difference between the two options and continue from there to find an upper bound of order $O(\Delta t)$... but how?.

$$0\leq C^{A} - C^{B} \leq ... \approx O(\Delta t).$$