Many risk-parity implementations simply use the

inverse-vol rule (i.e. weights are proportional to 1

over vol), and then all weights are (strictly) positive

by construction.

A number of implementations that do the full optimization

indeed set non-negativity as an

explicit constraint. But in general and without such

constraints, negative weights may occur when you

equalize risk-contributions (though negative weights

may be unlikely).

An example in R for a 4-by-4 covariance matrix, which is of rank 4 and positive definite:

S <- structure(c(0.000366309632978563, -0.000105943107569848,

-0.000119667135542588, 0.000169622848883779,

-0.000105943107569848, 0.000187730511335559,

-6.49497066288097e-05, -0.000167162505503921,

-0.000119667135542588, -6.49497066288097e-05,

0.000102201079006482, 1.88829418811814e-05,

0.000169622848883779, -0.000167162505503921,

1.88829418811814e-05, 0.000208993337170307),

dim = c(4L, 4L))

The implied correlation matrix:

cov2cor(S)

## [,1] [,2] [,3] [,4]

## [1,] 1.000 -0.404 -0.618 0.613

## [2,] -0.404 1.000 -0.469 -0.844

## [3,] -0.618 -0.469 1.000 0.129

## [4,] 0.613 -0.844 0.129 1.000

I do not use the riskParityPortfolio package, but it

seems to support negative weights, though the default is to not allow them:

library("riskParityPortfolio")

riskParityPortfolio(S)

## $w

## [1] 0.2313 0.2990 0.4588 0.0109

##

## $relative_risk_contribution

## [1] -1.9471 -0.0858 1.5197 1.5132

## ....

riskParityPortfolio(S, w_lb = -1)

## $risk_concentration

## [1] 1.93e-14

##

## $w

## [1] -0.0829 0.4391 0.2167 0.4271

##

## $relative_risk_contribution

## [1] 0.25 0.25 0.25 0.25

## ....

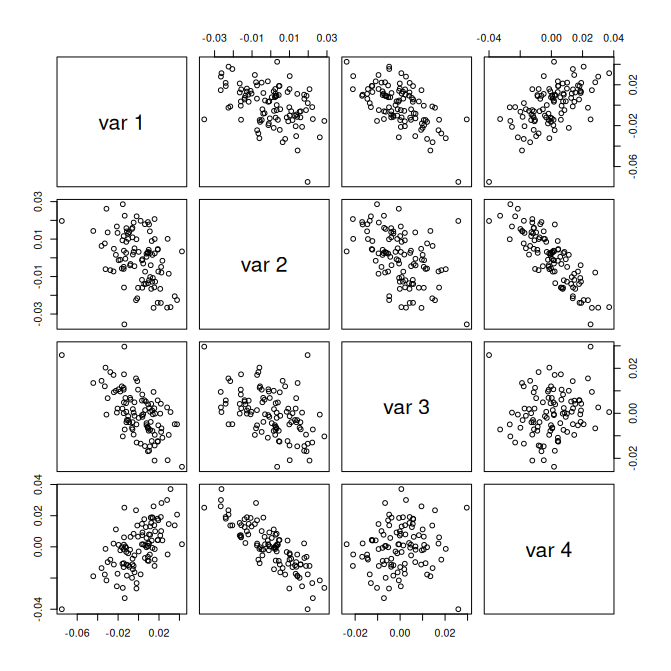

Additional note: The example covariance-matrix hides some fairly-strong dependencies between the asset returns, which may not be obvious from looking at the data:

library("NMOF")

R <- randomReturns(na = 4, ns = 100,

sd = sqrt(diag(S)),

rho = cov2cor(S), exact = TRUE)

pairs(R)

Computations based on such a matrix (such as a marginal-risk calculation) will typically be sensitive and react strongly to small changes ("perturbations") of inputs. In the example, you can get around this by increasing the iterations:

w <- riskParityPortfolio(S)$w

FRAPO::mrc(w, S)

## [1] -194.71 -8.58 151.97 151.32

w <- riskParityPortfolio(S, maxiter = 1e4)$w

FRAPO::mrc(w, S)

## [1] -67.3 11.2 78.2 77.9

w <- riskParityPortfolio(S, maxiter = 1e5)$w

FRAPO::mrc(w, S)

## [1] 23.1 24.7 26.1 26.1

w <- riskParityPortfolio(S, maxiter = 1e6)$w

FRAPO::mrc(w, S)

## [1] 25 25 25 25

(I use the marginal-risk function mrc from Bernhard Pfaff's FRAPO package.)

But of course, this is all the result of an empirical problem (not a computational one): the assets are highly-correlated, and so an algorithm will always have trouble differentiating between linear combinations of those assets.