I'm working through the implementation of a risk budgeting approach as described in the recent Roncalli paper. The idea is that the portfolio manager sets a contribution of total portfolio volatility to each asset in the portfolio (the budget, $b_i$ where $\sum_{i=1}^n b_i = 1$) and solves an optimization problem to find the weights ($x_i$ where $\sum_{i=1}^n x_i = 1$) of those assets that allow the assets' volatility contribution to match the set budget. A somewhat similar approach was discussed on this site here.

More formally (eq. 8):

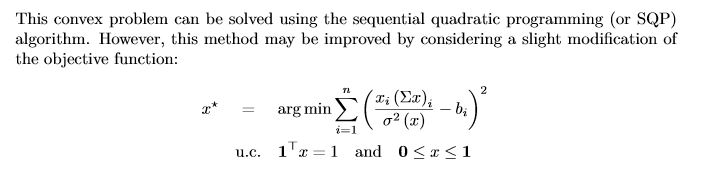

$$x^*=\underset{x}{\arg \min} \sum_{i=1}^n (\frac{x_i(\Sigma x)_i}{\sum_{j=1}^n x_j(\Sigma x)_j} - b_i)^2$$ $$u.c. 1^Tx=1; 0\le x \le 1$$

where

- $x$ is the weight of asset $i$

- $n$ is the number of assets

- $(\Sigma x)_i$ is the covariance of asset $i$ wrt to the portfolio (I think this is the interpretation, perhaps someone can confirm)

- $b_i$ is the set risk budget for asset $i$

What I am trying to do is add to this approach the ability for the manager to set an overall target portfolio volatility in addition to the budget of each asset.

According to the paper, we know:

$$\sum_{i=1}^n RC_i(x_i,...,x_n)=\sum_{i=1}^n x_i \frac{(\Sigma x)_i}{\sqrt{x^T\Sigma x}}=\sigma(x)$$

where

- $RC_i$ is the risk contribution ($b$) of asset $i$

Because of these relationships, I've drawn the conclusion that $\sqrt{x^T\Sigma x} = \sum_{j=1}^n x_j(\Sigma x)_j$ (portfolio volatility is the sum of each assets' volatility contribution), I thought I might insert my target portfolio volatility as the denominator of the minimization problem above. I got reasonable results in my tests but the actual portfolio volatility using the results of the optimization problem never matched the target.

After I thought about this for a while, I realized this approach is probably naive and likely wrong. Basically, because I'm using two different covariance matrixes to represent the same volatility value: the computed covariance matrix included in the numerator and the covariance matrix that is implied by a target volatility estimation.

My question is twofold:

- Are there papers/references available that describe the mechanics of setting asset level risk budgets as well as a portfolio level target volatility?

- Does anyone have an idea independent of any papers or resources how I might go about setting asset level risk budgets as well as a portfolio level target volatility?