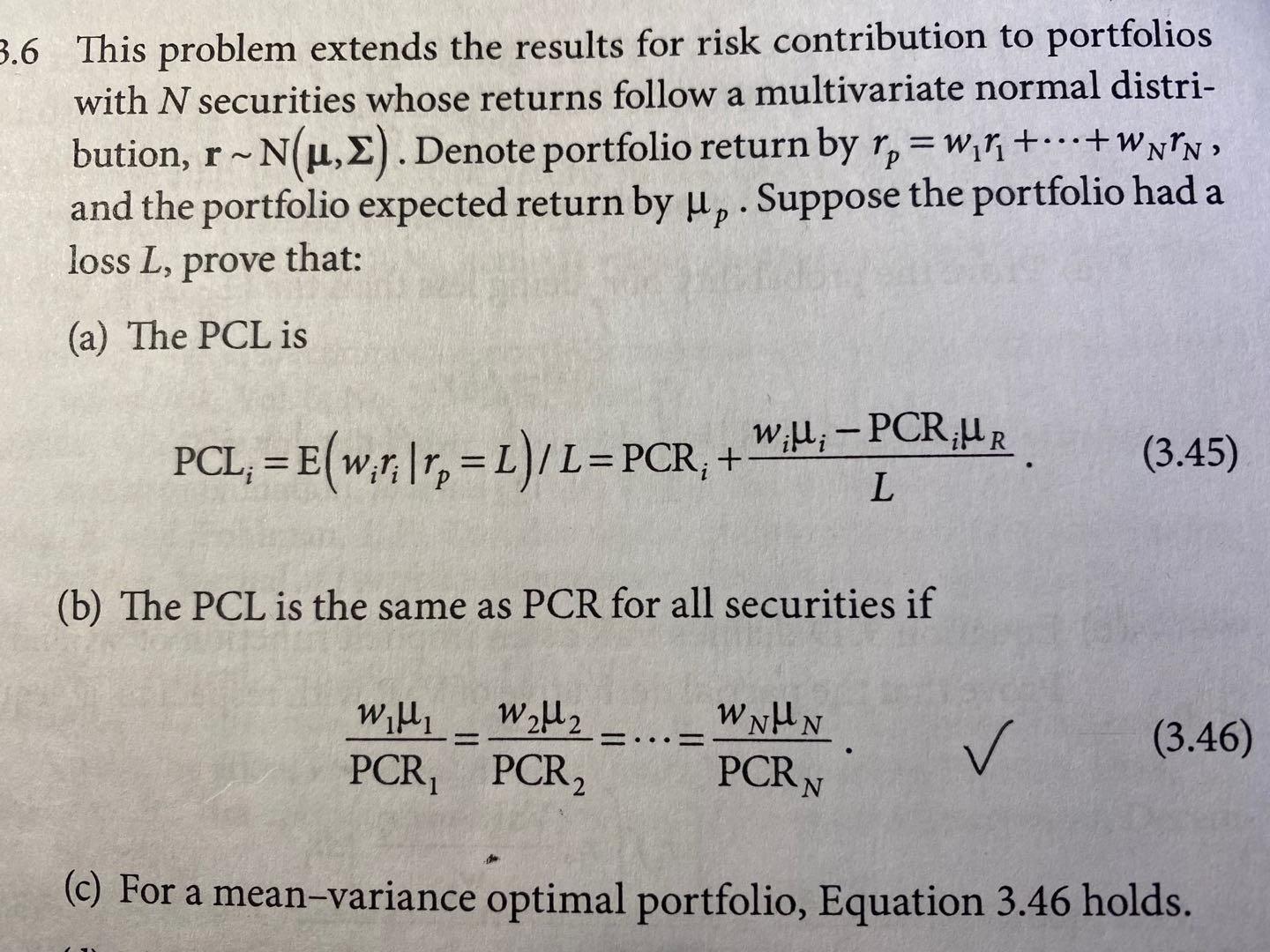

I came across this question during self study on a quantitative book (Question 3.6 on Page 75 of Quantitative Equity Portfolio Management: Modern Techniques and Applications By Edward E. Qian, Ronald H. Hua, Eric H. Sorensen ), can someone help me out? I got stuck on part(c). FYI, PCR = Percentage Contribution to Risk, PCL = Percentage Contribution to Loss, the definition for PCR is: $$PCR_i=\frac{\omega_i\frac{\partial\sigma}{\partial w_i}}{\sigma}$$ and I have already found the optimal $\displaystyle \omega^*$ and optimal $\displaystyle (\sigma^*)^2$ from mean-variance optimization problem formed as follows. $$Maximize \ \ \ \ \ \ \omega^T\cdot f-\frac{1}{2}\lambda(\omega^T\Sigma\omega )\\ subject \ \ to \ \ \ \ \ \ \omega ^T i=1$$