All the parameters of the solution need to be estimated for your specific stock. Stochastic process-specific parameters, i.e. $\mu$, $\sigma$, have to be estimated by some classical method (e.g. MLE, minimum contrast, etc.). No parameter of tick size is incorporated in the model, you will have to decide at the end whether the in-between quote shall be assigned to the higher or lower price value. And parameters relating to the order arrival need to be estimated similarly as derived in the original paper of Avellaneda & Stoikov. There you may find the derivation from three separate formulas:

Constant frequency $\Lambda$ of market buy/sell orders estimated by dividing the total volume traded over a day by the average size of market orders on that day.

The distribution parameter of the size of market orders

$$

f^{Q}(x) \propto x^{-1-\alpha}

$$

where $\alpha$ will be overtaken from the literature (presented in the original study), or else needs to be calculated from your specific dataset.

- Temporary impact of a large market order:

$$

\Delta p \propto ln(Q),

$$

also either overtaken from the literature or estimated on the historical values of your specific stock.

By putting all these three formulas together, you obtain the original result:

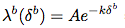

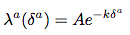

$$

\lambda(\delta) = Aexp(-k\delta),

$$

where $A = \Lambda / \alpha$ and $k = \alpha K$, $K$ being a scaling parameter for the temporary impact of a market order.

Source: Avellaneda, Marco, and Sasha Stoikov. "High-frequency trading in a limit order book." Quantitative Finance 8.3 (2008): pp. 220.

https://www.math.nyu.edu/faculty/avellane/HighFrequencyTrading.pdf