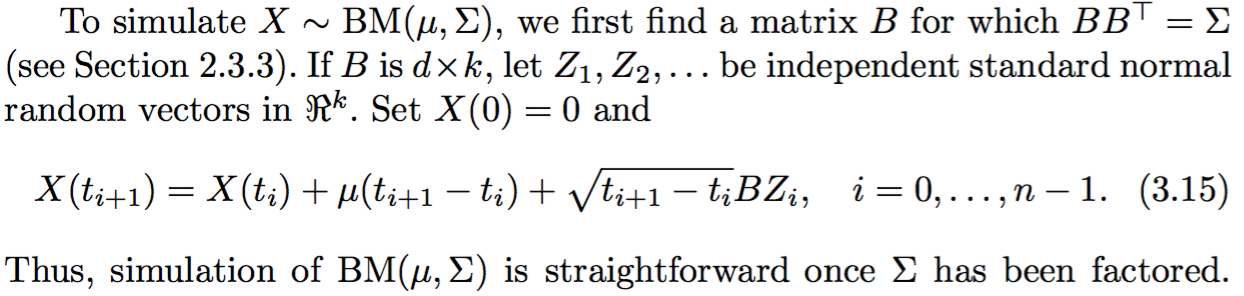

A topic I am struggling with is the implementation of a (for the simplest higher dimensional case) bivariate normal distribution simulation for geometric brownian motion. The clearest explanation by far I've been able to find is within Glasserman's Monte-Carlo Methods in Finance book, and this is what it says:

I understand that the covariance matrix $\Sigma$ of the two normal distributions needs to be provided (which is simple based on some sample date), and that $Z_i$ is a normal variable that needs to be numerically generated, but how would I go about incorporating the above into the standard GBM formula for generating a sample path? $$S_i = S_{i - 1} \exp\left\{ \left( r - \frac{1}{2}\sigma^2 \right) \Delta t + \sqrt{\Delta t} Z_i \right\}$$,

where $\Delta t = T / n$ and $n$ is the number of intervals.

I seriously do now know where to begin, so if some of you could give me pointers as how to approach this seemingly typical simulation demand, I would be very grateful.