Suppose we assume that yields on a zero-coupon bond that matures at time $T$ follow a log-normal process of the type $y(t,T)=y(t_0,T)e^{-0.5\sigma^2t+\sigma W_t}$ under the T-forward measure.

Then, I could express the price of the zero-coupon as: $$P(t,T)=\frac{1}{(1+y(t,T))^{T-t}}$$

For simplicity assume $T-t=n$ where $n$ is some integer.

Is there a name for the distribution of the Bond price for various $n=1,2,..$ ?

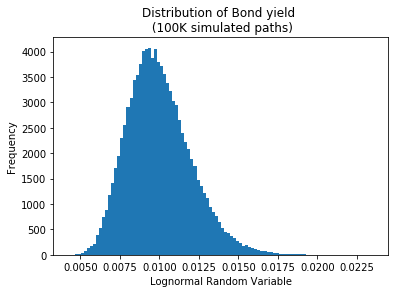

Setting the initial yield to 1%, and running 100K paths, the yield histogram looks like a log-normal distribution (as - of course - expected):

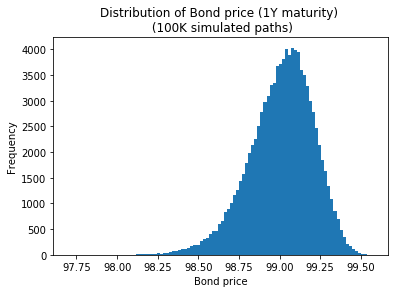

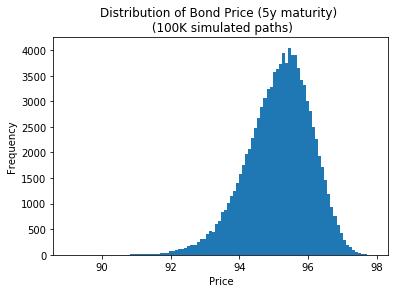

Plotting the Bond price (charts below) sort of looks like "log-normal rotated around its mean" (scaled to a different scale than the yield): does it have a name and a well defined PDF?

My final question (I don't have a lot of experience with pricing Bond options): could the above assumptions (i.e. log-normal yields under the T-forward measure) be used to price a bond option of the type:

$$C_{T_1}=\mathbb{E}^{Q_T}\left[ (P(T_1,T)-K)^{+} \right]$$

What would be the industry standard nowadays for pricing a bond option such as the above, with regard to the price process assumed for the bond price? (would the industry standard be different to assuming the yields are log-normal and modeling the Bond price via the yield as above?)