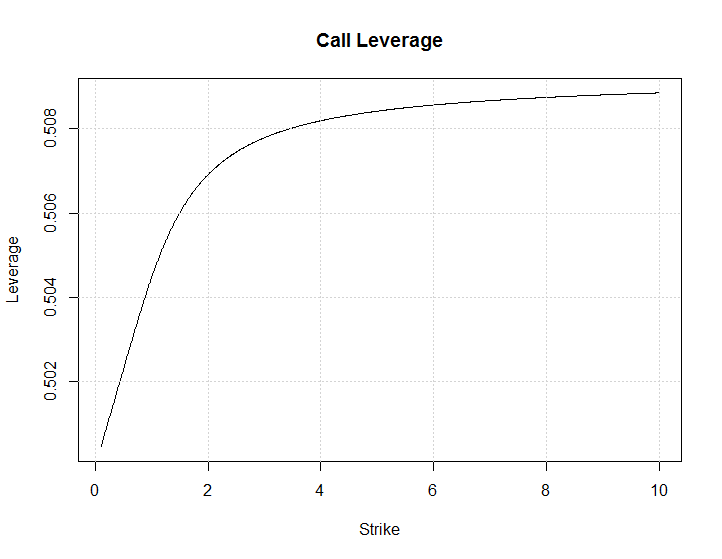

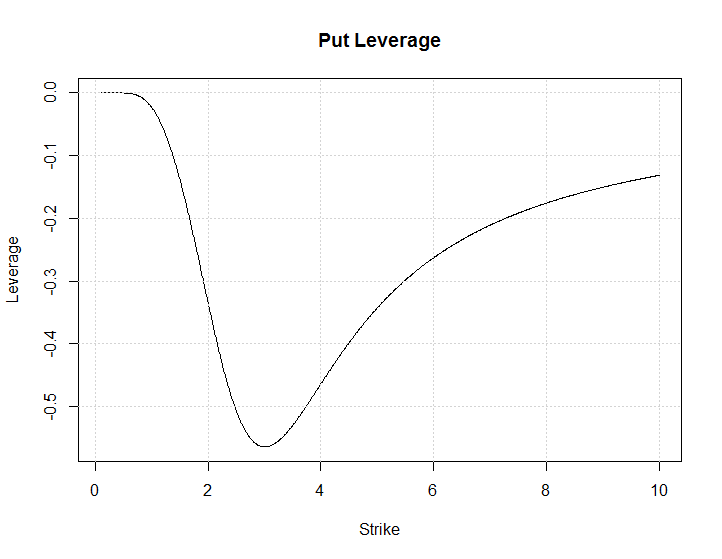

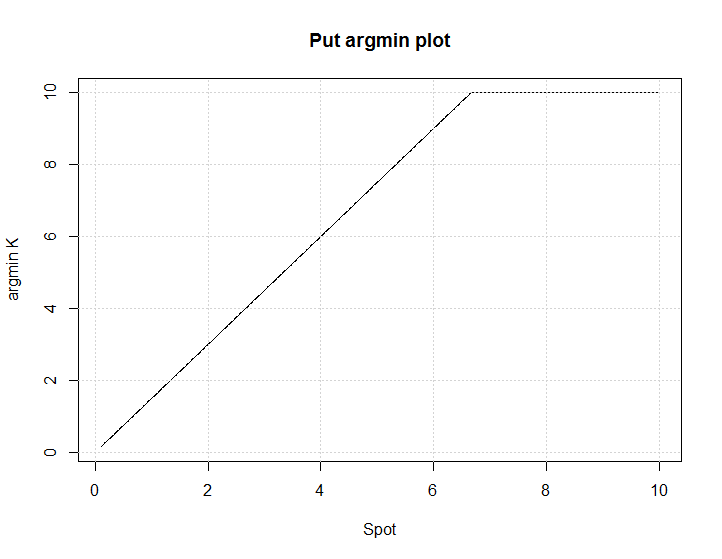

Since options represent leveraged stock investments, at which strike $K$ does a European option provide maximum leverage?

Hereby define leverage $L$ as ratio of Delta/Optionprice:

$$L(K)=\frac{\Delta(K)}{C(K)}$$

You can assume all parameters fixed and positive ($T-t>0$) except strike $K (>0)$.

Delta is defined as $\Delta=\frac{\partial C(S)}{\partial S}$.

The maximum option leverage strike is important as it provides the maximum possible profit (and loss) on investment.

Numerical solutions would be acceptable (e.g. MATLAB fmincon).

Graphical solutions would also be acceptable (e.g. MATLAB plot or http://www.wolframalpha.com/input/?i=x%5E2).

Intuitive explanations would be acceptable.

For theoretical solutions you can use Black-Scholes model where

\begin{align} C(S, t) &= N(d_1)S - N(d_2) Ke^{-r(T - t)} \\ d_1 &= \frac{1}{\sigma\sqrt{T - t}}\left[\ln\left(\frac{S}{K}\right) + \left(r + \frac{\sigma^2}{2}\right)(T - t)\right] \\ d_2 &= \frac{1}{\sigma\sqrt{T - t}}\left[\ln\left(\frac{S}{K}\right) + \left(r - \frac{\sigma^2}{2}\right)(T - t)\right] \\ &= d_1 - \sigma\sqrt{T - t} \end{align} and \begin{align} P(S, t) &= Ke^{-r(T - t)} - S + C(S, t) \\ &= N(-d_2) Ke^{-r(T - t)} - N(-d_1) S \end{align}

The deltas for call and put are

$$\Delta^C=N(d_1)$$ $$\Delta^P =N(d_1) - 1$$

where $N(\cdot)$ denotes the cumulative Normal distribution.