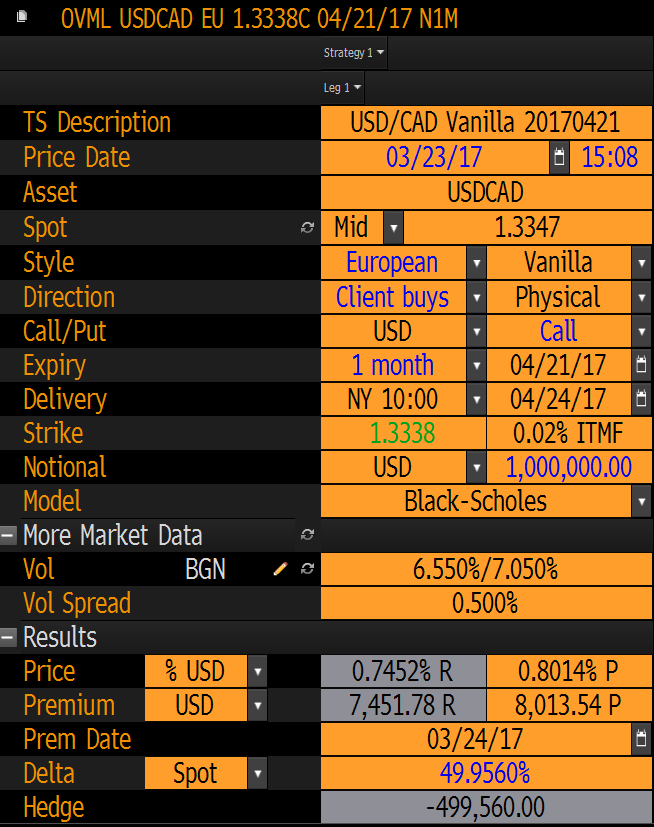

To understand how Bloomberg prices foreign exchange vanilla options , I extract the following screenshot from its OVML function.

The Black-Scholes formua for vanilla options are \begin{split} & P=\phi\big(Se^{-R_fT}N(\phi d_1)-Xe^{-R_dT}N(\phi d_2)\big) \\ & d_1 = \frac{\ln(\frac{S}{X})+(R_d-R_f)T+0.5\sigma^2T}{\sigma\sqrt{T}} \\ & d_2 = d_1-\sigma\sqrt{T} \end{split} where

$\phi$: 1 for call; -1 for put

$S$: Spot rate

$X$: Strike rate

$R_d$: Domestic interest rate

$R_f$: Foreign interest rate

$\sigma$: Volatility

$T$: Time horizon

From the screenshot, I get

\begin{split} & S = 1.3347 \\ & X = 1.3338 \\ & T = \frac{22}{252} = 0.08730 \text{ yrs} \\ & \sigma = 0.0655 \end{split}

I also look up that the $R_{USD} = 0.75$ and $R_{CAD}=0.50$. Plugging these numbers in, I get

$d_1 = \frac{\ln(\frac{1.3347}{1.3338})+(0.75-0.50)\times 0.08730+0.5\times 0.0655^2 \times 0.08730}{0.0655 \sqrt{0.08730}} = 1.5580$

$d_2=1.5580 - 0.0655*\sqrt{0.0873} = 1.5386$

and $P = 1.3347 \times e^{0.50\times 0.0873}\times N(1.5580) - 1.3338\times e^{-0.75\times 0.0873}\times N(1.5386) = 0.03864$, which is nowhere close to Bloomberg's result of 0.07452.

I also tried multiplying volatility by $\sqrt{12}$, assuming that the volaility they gave is monthly not annualized. The resulting price is 0.05624, which doesn't match either.

I also tried changing 0.75 and 0.5 into 0.0075 and 0.005, assuming that the interest rates are in percentages. The resulting price is 0.01688, which also doesn't match.

What am I missing?