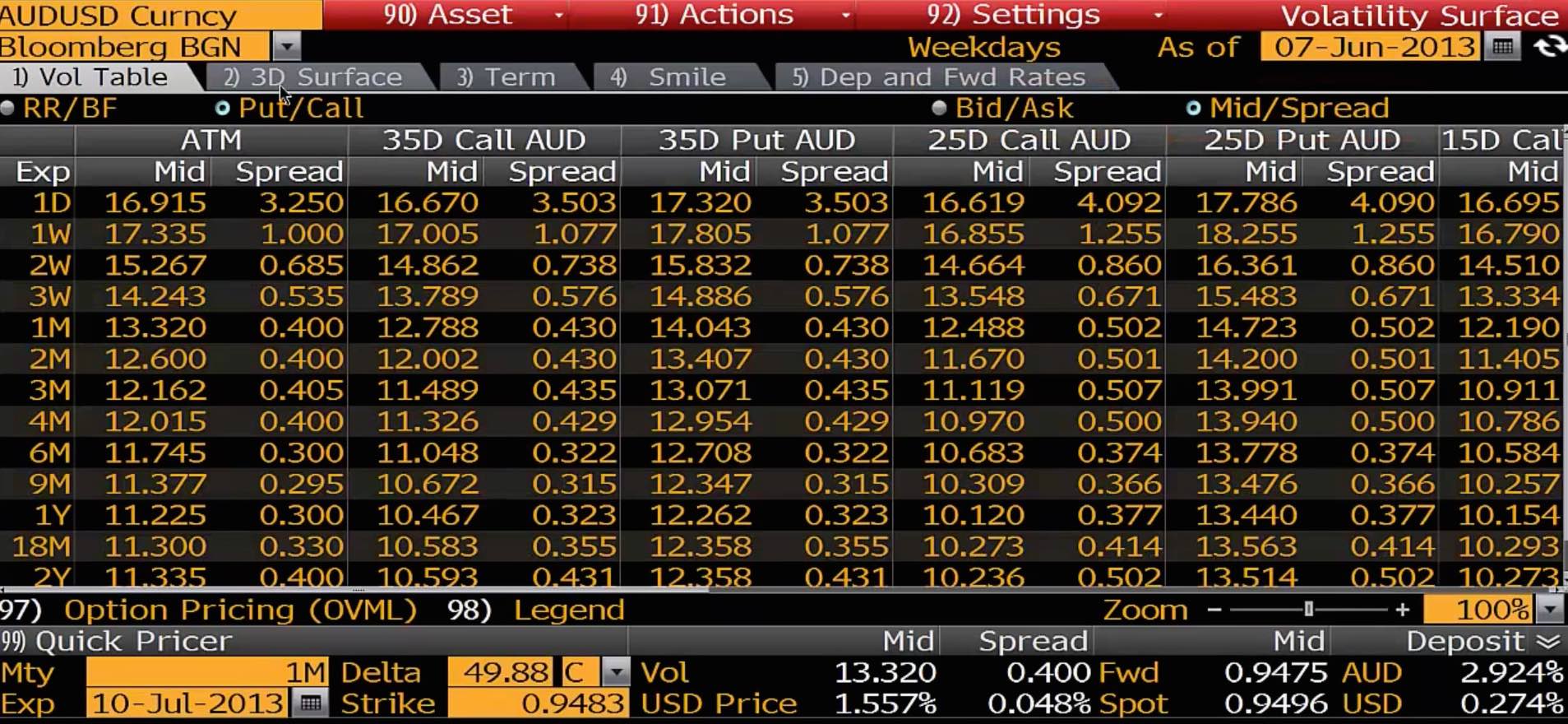

I am trying to find out how to go from delta to strike. If we look at the Bloomberg I am looking at 1M ATM volatility. I have included the Bloomberg data as a picture where we have following information: $f=0.9475$, $r=0.00274-0.02924$, $\sigma =13.32/100$, $T=1/12$, $t=0$.

The strike for $delta=0.4988$ appears at the picture as well, and I try to recreate it. I use definition for the Black Sholes delta and I have this problem now:

$d(k)=\frac{1}{\sigma \sqrt{T-0}}*\text{Log}\left[\frac{f}{k}\right]*\left(r+\frac{\sigma ^2}{2}\right)*(T-t)$, $r_f=0.00274$

$ SOLVE[e^{r_f*(T-t)}*N\left(d_1(k)\right)=0.4988]$ , $ k = 0.950417$

According to bloomberg this correct answer is $k=0.9483$. What went wrong? Personally I believe it's dates and time parameters that's not correct. According to Bjork: Arbitrage Theory in Continuous Time the time parameters need to measured in years. And in general. Is my approach correct?

I have found out about this method by looking at topics that are discussed here: Calculate strike from Black Scholes delta

Black model: Delta - strike relationship regardless of expiry?