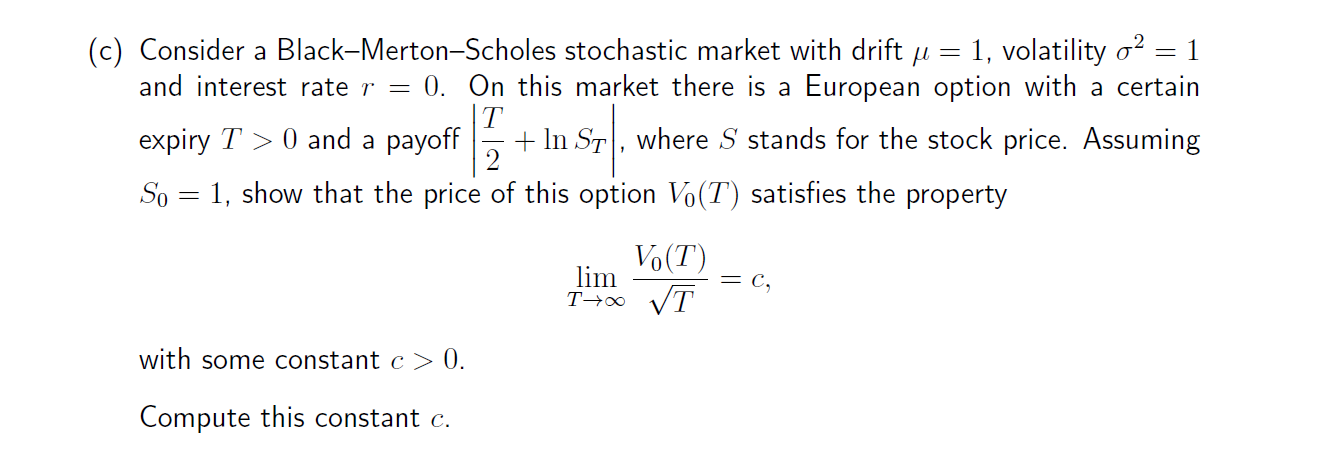

The following image shows a past exam question that I am attempting to answer (for which I do not have a mark scheme):

I believe that under the BMS model, the payoff of a stock at maturity $T$ is given by $$ S_T = S_0 \exp \left( \mu T + \sigma W_T \right) $$

Thus, the payoff of the stock in the question would be given by $$ S_T = \exp \left( T + W_T \right) $$

Therefore, I would expect the payoff of the option to be $$ V_0 (T) = \left| \frac{T}{2} + T + W_T \right| = \left| \frac{3T}{2} + W_T \right| $$

However, $$ \lim_{T \rightarrow \infty} \frac{\left| \frac{3T}{2} + W_T \right|}{\sqrt{T}} = \lim_{T \rightarrow \infty} \left| \frac{3\sqrt{T}}{2} + \frac{W_T}{\sqrt{T}} \right| = \infty $$

What am I doing wrong?