I am trying to understand the Avellaneda-Stoikov model for high frequency trading, in particular the optimizing agent with infinite horizon.

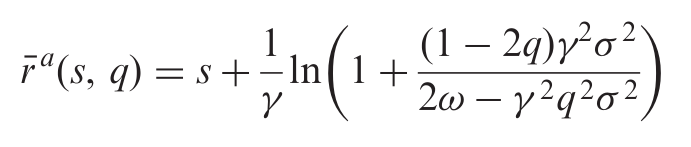

The reservation ask/bid prices for such an agent are defined in the paper as:

and

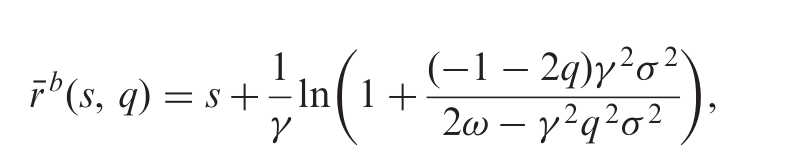

and

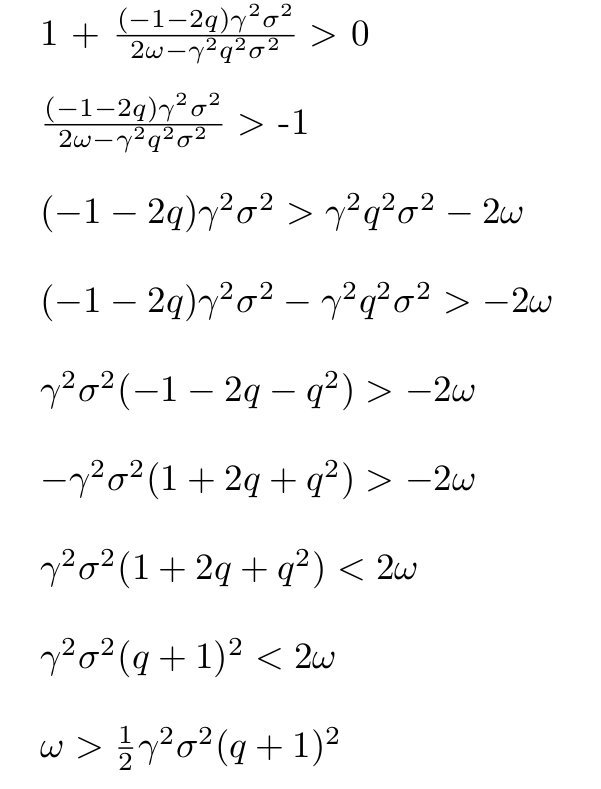

It is said in the paper that $\omega$ serves as an upper bound on the inventory position.

It is said in the paper that $\omega$ serves as an upper bound on the inventory position.

I took the argument of the natural logarithm from the reservation bid price and wrote the inequality satisfying the logarithm:

Looking closer at the formula for $\omega$, we see that it depends on some $q_{max}$ parameter.

What I can't answer for myself is the question whether $q_{max}$ is heuristically chosen or is it estimated by some established method.