I'm currently backtesting a mean reversion pairs trading strategy. However, instead of simple long or short trading signals, I'm using multiple "levels", where the further away the spread is from the mean, the more positions I put on.

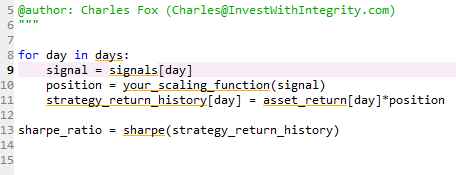

However, since the Sharpe Ratio (and other performance metrics) only use percent returns, it only captures whether or not I'm in or out of the market, since regardless of whether or not I'm holding 1 or 10 positions, the percent return is the same.

Is there a way to calculate the Sharpe Ratio while accounting for dynamic position sizing? If not, are there any risk-adjusted performance measures that are able to capture this behavior?

I was thinking of weighting the mean and standard deviation of the daily returns based on the number of positions for each day, but I'm not sure if that's the right approach.