I am trying to understand the interrelations between the marginal, cumulative and conditional PDs (Probabilities of Default) when modelling ECLs (Expected Credit Losses). My current understanding is that for a loan with remaining maturity of $t$ years the following calculations apply:

Conditional $PD_{t} = (PD_{t}|PD'_{t-1})$

Marginal $mPD_{t} = PD_{t}*(1-PD_{t<n})$

Cumulative $cPD = \sum_{t=1}^{n} mPD_{t}$

Alternatively $mPD = cPD_{t}-cPD_{t-1}$

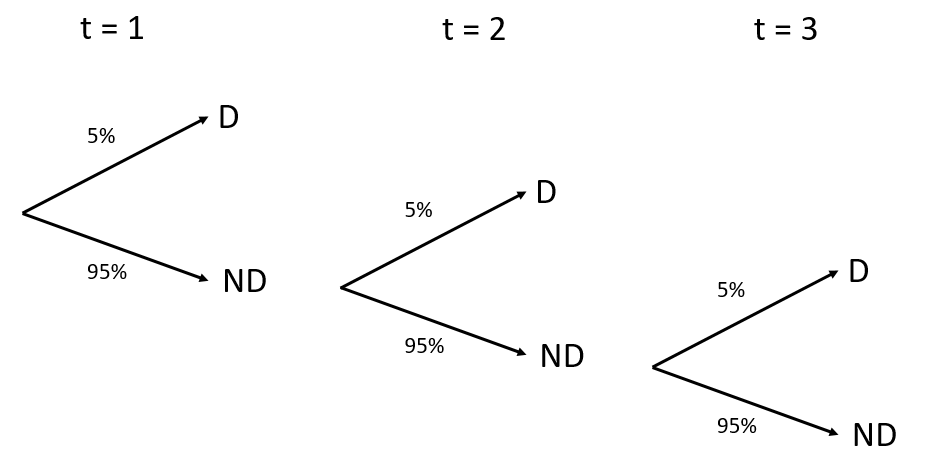

A numerical example would be as follows:

$t = 3$

$PD_1 = 5\%$ for simplicity we we assume independenceso that $PD_{t} = PD_{t-1}$, which gives us the following tree diagram:

From the diagram it follows that:

From the diagram it follows that:

$mPD_{1}=5\%$

$mPD_{2}=5\%*95\% = 4.75\%$

$mPD_{3}=5\%*95\%*95\% = 4.51\%$

$cPD_{1} = 5\%$

$cPD_{2} = 5\%+4.75\%=9.75\%$

$cPD_{3} = 5\%+4.75\%+4.51\%=14.26\%$

My question is what numbers should be applied when modelling ECLs. For example if we have a 3 year loan for 1m USD at 5% interest (for simplicity lets assume that the payments are made annually) then the annual payments will be 367,208 USD. So if we want to calculate the ECLs for this loan do we need to apply the marginal or conditional probabilities? And to what to we apply these probabilities to, the cash flows or the remaining balance of the loan?