With dividends, $$d1 = ( log(S/K) + (r - d + 1/2*σ^2)*t ) / (σ*sqrt(t))$$

which is identical to

$$d1 = ( log(F/K) + 1/2*σ^2*t ) / (σ*sqrt(t))$$

because the forward is computed $F = S e^{(r-q)T}$

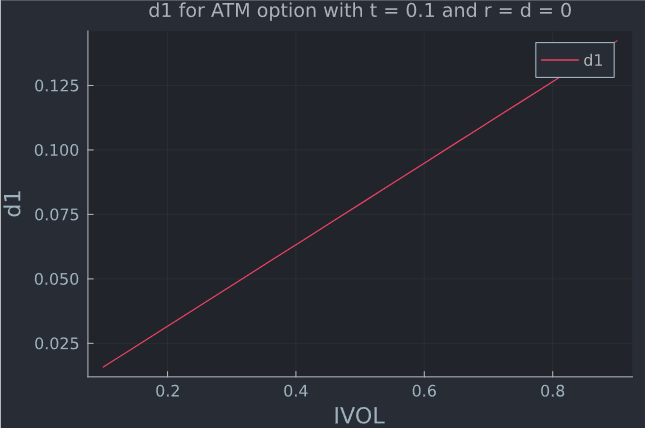

Using this, setting $r = d = 0$ will result in delta being > 0.5 for any time $t$ and implied vol $\sigma$ that is > 0 (hence all the time). This comes from the fact that if $d1 =( log(F/K) + 0.5*σ^2*t ) / (σ*sqrt(t))$, you can see that for 100% moneyness, hence $F=K$, $d1>0$ which means it is above 50D which corresponds to N(0.0). It is an increasing function of vol:

and the term

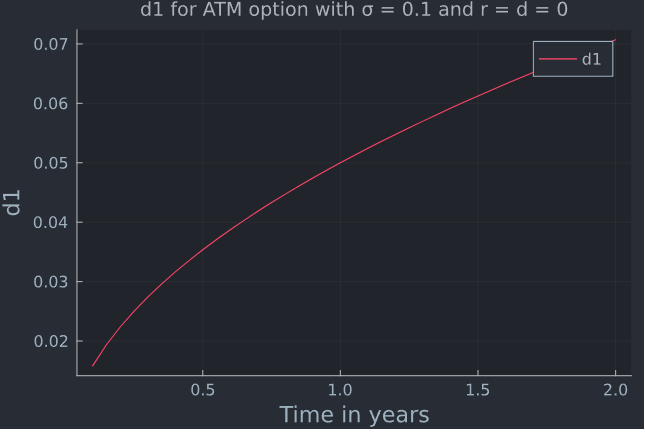

$$\frac{log(\frac{F}{K})}{\sigma\sqrt t}$$ in d1 converges to 0 as $t \rightarrow \infty$ (the larger vol, the quicker it converges), which leaves us with $1/2∗σ2∗t$ which in turn is growing withough bound in $t$ and $\sigma$.

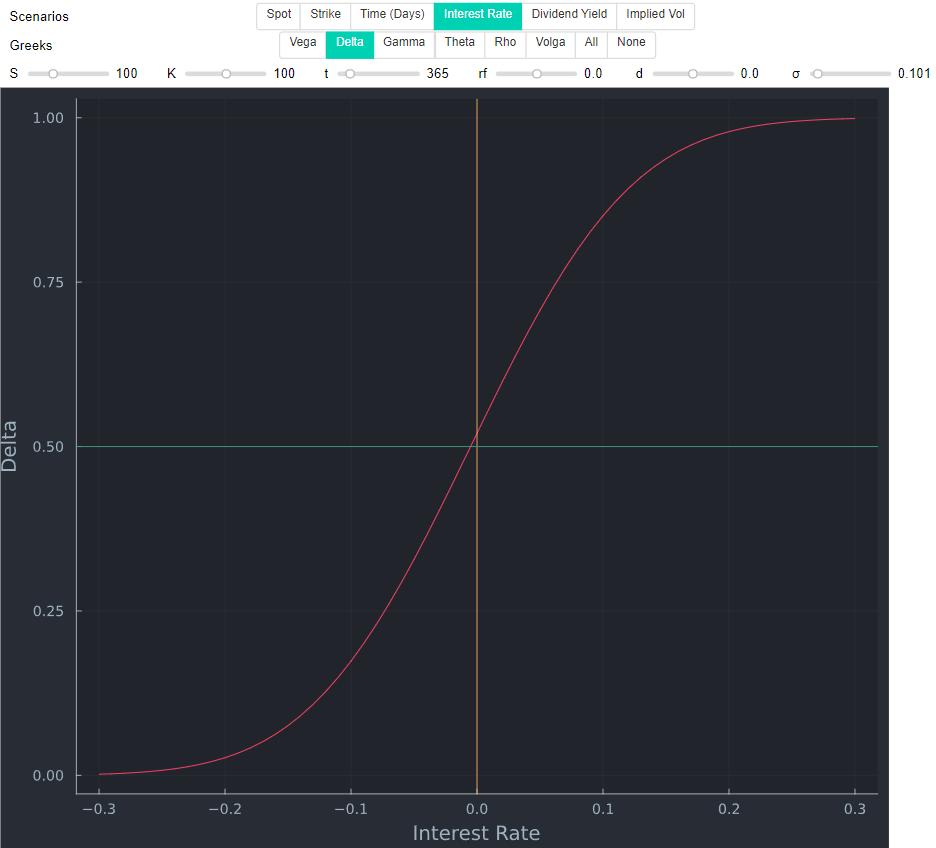

With interest rate and dividends, it depends on the forward, just like @Richi W explained. In the following App I made in Julia, I price an ATM option, with 365 days to maturity, and an IVOL of 10%. The horizontal axes shows different interest rates, and dividends are set to 0. The vertical line shows the zero interest case and on the horizontal line corresponds to 0.5 delta. You can clearly see how different interest rates affect delta for an ATM option.

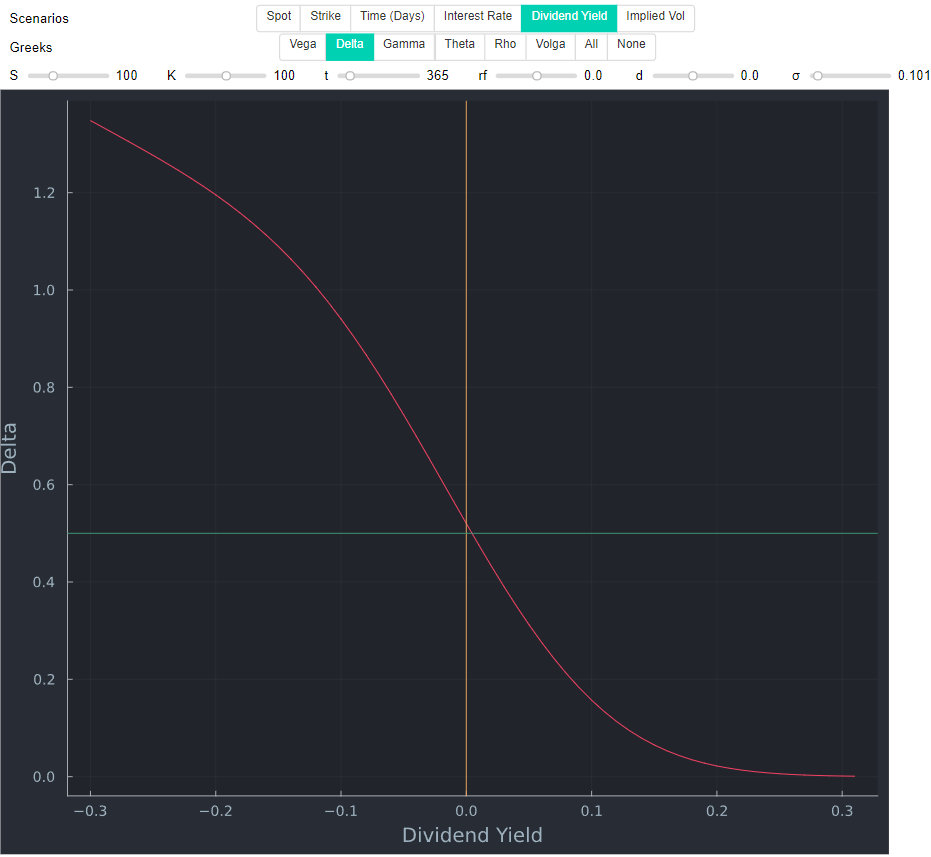

The same (in opposite direction) is true for different dividends (for convenience, rates are set to 0).

Last but not least, the risk-adjusted probability of the event that the option will finish in the money is P(ST>X)=N(d2), as shown in Understanding N(d1) and N(d2): Risk-Adjusted Probabilities in the Black-Scholes Model by Lars Tyge Nielsen for example. Contrary to another answer, this is also not a constant of 0.5 for ATM options but tends to 0 if $t \rightarrow \infty$ and / or $\sigma \rightarrow \infty$ as shown in this answer.