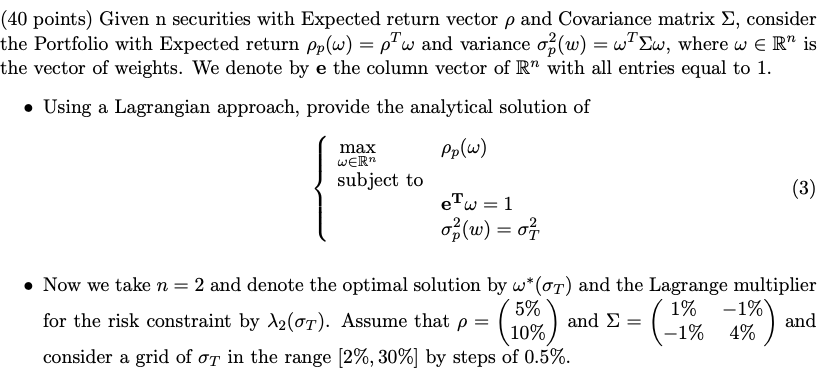

I understand Markowitz and targeting returns to minimize our variance. I know this optimization problem well and its constraints. However when the reverse scenario is to be considered I get very confused. How do I mathematically show optimal portfolio weights when I want to target my variance to maximize my return?

I am supposed to use a Lagrangian method but all I get is lambda in relation to some optimal weight. I know that the optimal variance condition should be 1Tranpose * covariance matrix * 1 where 1 is the ones matrix. I can mathematically show this but cannot understand how this optimal variance relates to the optimal weights and portfolio return.