I am looking for caplet implied volatility data for Libor-EUR. Is there any online data base etc. available to get such data? Does Bloomberg offer this data?

Any pointer will be highly appreciated.

Many thanks,

I am looking for caplet implied volatility data for Libor-EUR. Is there any online data base etc. available to get such data? Does Bloomberg offer this data?

Any pointer will be highly appreciated.

Many thanks,

VCUB will not show caplet vol but shows cap vol (as one of the inputs). Caplets are a sequential series of interest rate options (that together form the cap). You need cap stripping to extract the volatilities of individual caplets implied by the quotes of the caps that consist of them. Do you really need the caplets directly?

Since you have access to BBG - you can look at HELP VCUB - "Documents" for the "Bloomberg Volatility Cube" white paper. It explains cap stripping on P.9 onwards.

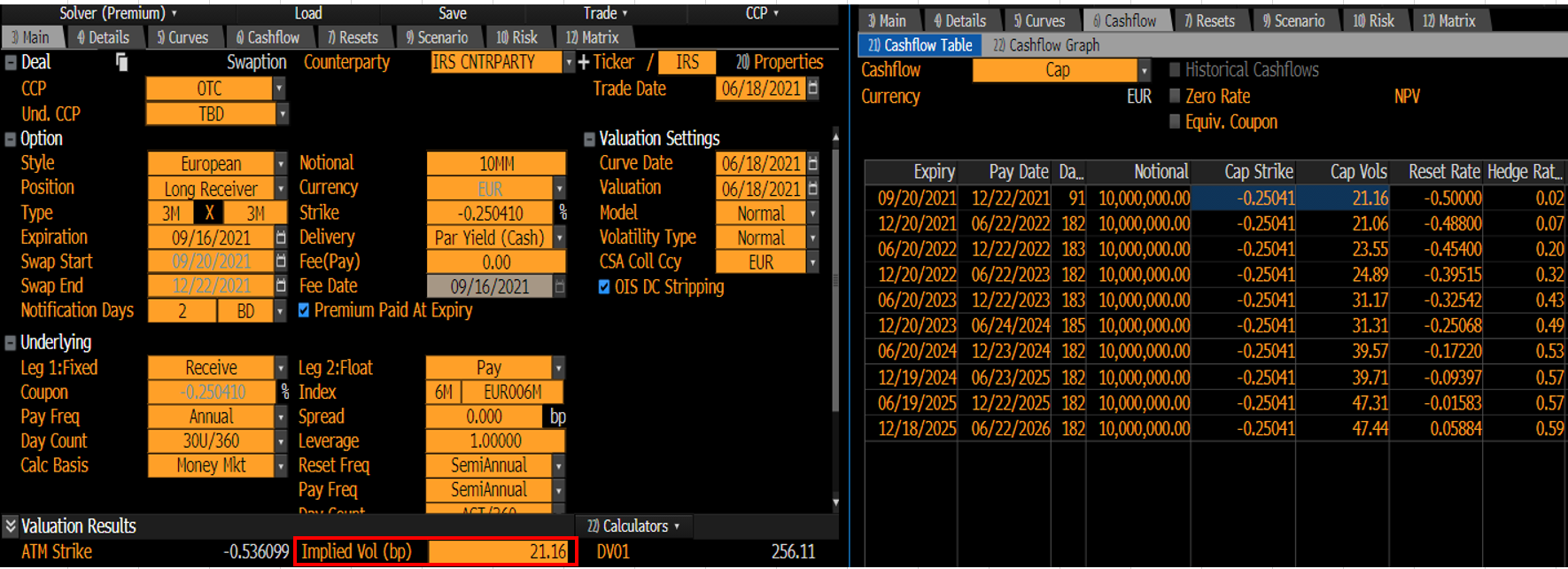

To directly see the caplet vols for a given cap, you can run SWPM -CAP EUR - click on the "cashflow" tab - you see a column called "Cap Vols". The main tab only shows the cap vol itself, that it is the flat vol which, when used as optlet vol in cap pricing, gives the deal the same premium. Caplet pricing uses swaption vol since each optlet can be seen as a one period swaption. So caplet vol is swaption vol (for given expiry and swap end as well as strike).

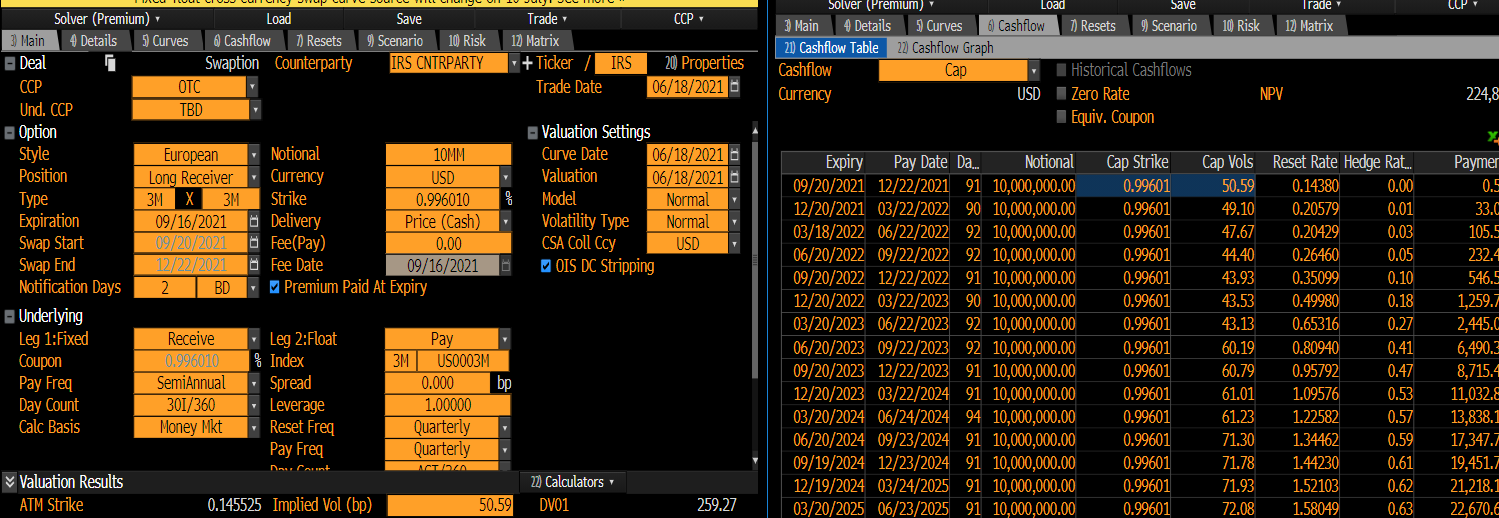

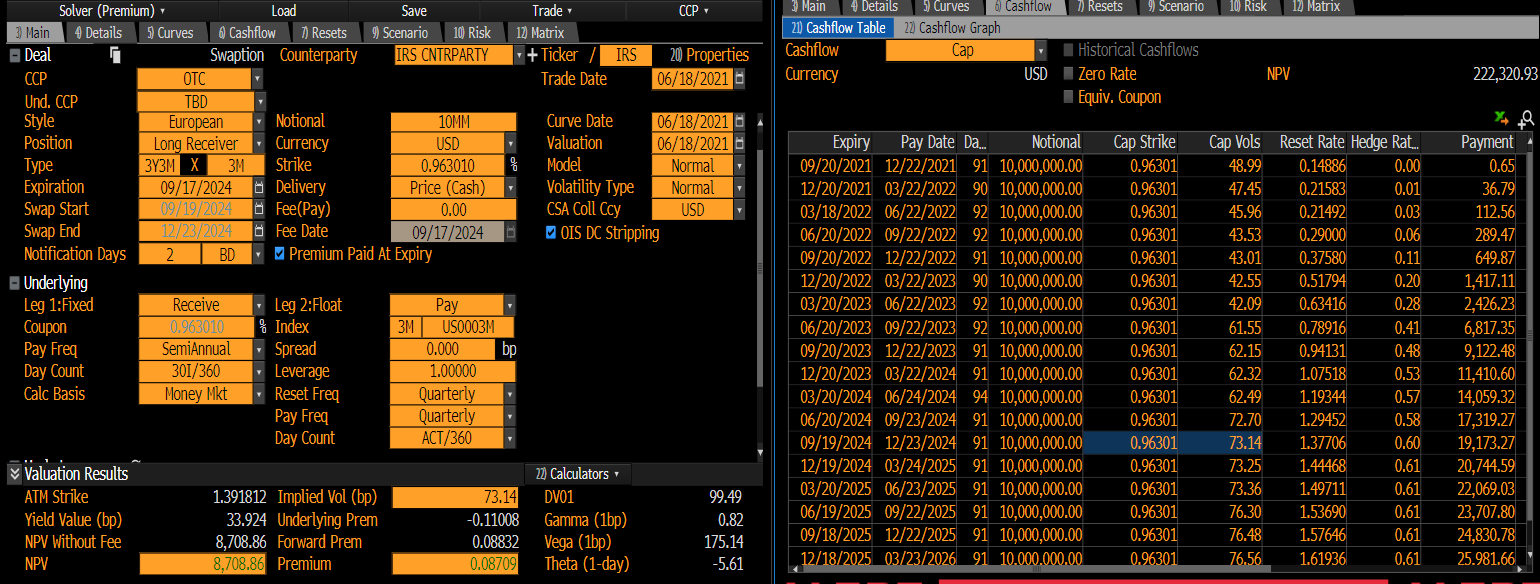

Same for US

Same for US

This also explains why the scenarios on SWPM and MARS (defined in SHOC) only shift the "interest rate vol" and not cap vol (hence the stripped VCUB vol). With EUR, you generally have an additional issue, because the Euro market trades caps as 3m-based below 2y maturity and 6m-based thereafter.

ICAP data can also be found on the terminal by typing VOLS in the command line - "25 ) Caps/Floors Vols" (at the time of writing). There are several contributor pages on CTRB - e.g. Tullett Prebon -> Int Rate Volatility -> Spot Caps -> Norm Vol -> EUR vs 6m -> Digital GDCO 3096 4 for the (current) direct link.

Do you really need the caplets directly?

$\endgroup$

Commented

Jun 19, 2021 at 19:18

If you have a Bloomberg terminal, you can lookup vols for different currencies and indexes with the VCUB function, where you can check the raw market input data and the surface construction parameters (vol type, interpolation, calibration, tenors, etc) and output.

You will have to have a Bloomberg licence because they don't really "offer" this data for free. Also, you'll have to be careful will what you do with the data, because the normal licence includes the data for personal use and you cannot share this data or, in some cases, produce numbers based on the data to publish to others.

There are also data licensed to have access to data only. Bloomberg has this but probably also brokers like ICAP.