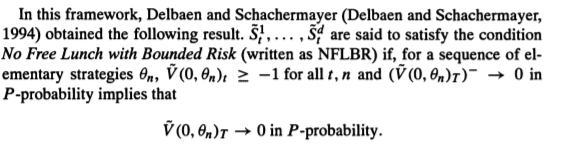

I am reading a book which states 'No free lunch with bounded risk as follows

where $\tilde{V}_t$ is the discounted value of the portfolio.Then it states the following theorem

EMM is the equivalent martingale measure.

But Wikipedia states the same theorem in the following way

Does this mean that the two conditions No free lunch with bounded risk and No free lunch with vanishing risk are equivalent. If yes how can I show it.