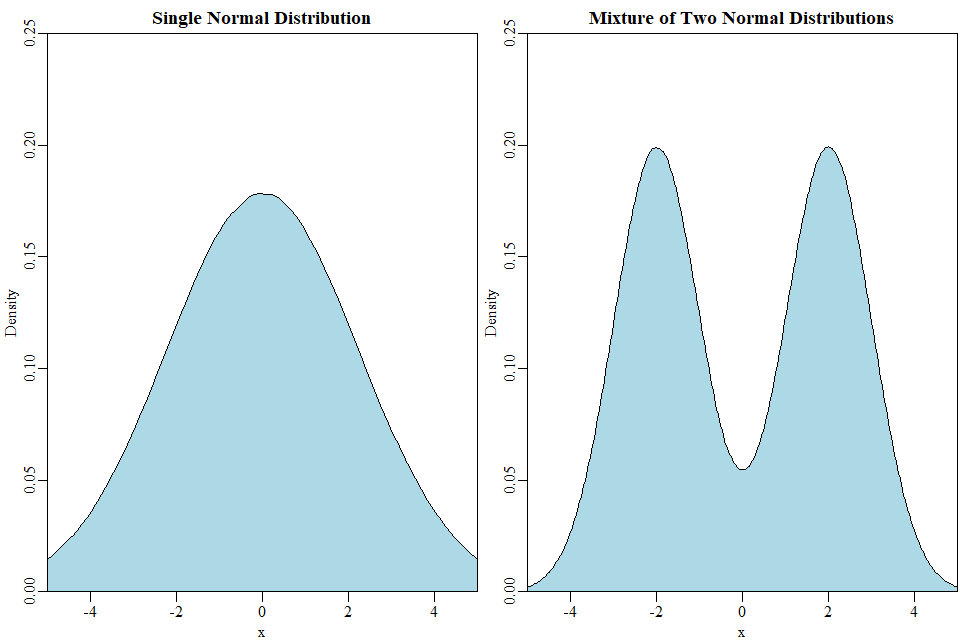

In making a choice among financial strategies, each of which has some estimated return distribution, some strategies will clearly be better than others. But many times, the choice is a question of risk tolerance. That said, there's still a problem: the risk/reward tradeoff is often too coarse -- because different distributions (e.g., outputs from a monte carlo simulation) may have the same mean and standard deviation while being qualitatively different (e.g., see image below).

Is there any more general, principled way to compare arbitrary probability distributions of expected returns? Like defining some kind of (maybe multi-dimensional) pareto curve over PDF space? Or another quantitative technique to make this selection process more rigorously grounded?

Given a set of modeled strategies, and return distributions like these ones, how can we identify the set of "dominating" distributions that are "best" in some sense? How can we rigorously guide the selection among them?