This may be a trivial question, but one I wasn’t sure about. Imagine I want to buy a 1 year ATM straddle. Does “at the money” imply buying closest to the current spot price, or does it mean to buy at the strike closest to the forward price. Was curious because I was looking at some option chains and for longer maturity options the spot ATM is something like 60/40 deltas rather than 50/50, which is usually a couple strikes higher.

1

-

2$\begingroup$ In which asset class? $\endgroup$– user42108Commented Jul 6, 2021 at 15:35

Add a comment

|

3 Answers

$\begingroup$

$\endgroup$

3

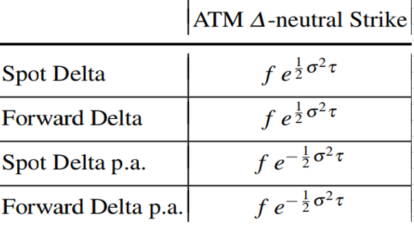

I guess generally what ATM means depends a lot on asset classes. FX vols are quoted as ATM DNS (delta neutral straddles). This in itself can be Spot, Forward, Spot premium adjusted, forward premium adjusted with the following formulas retrieved from the working paper FX volatility smile construction :

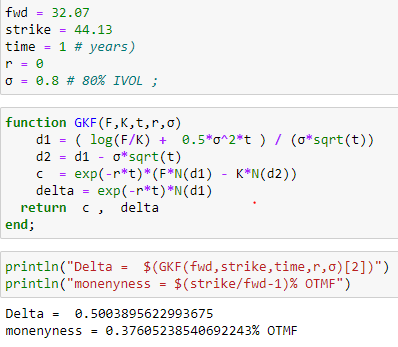

However, based on your wording I assume you think 50D would be ATM. That is just a common misconception. Since you write option chains, I assume it is listed and not FX stuff. If you for example look at commodity, these are usually options on futures. Hence modelled with Black76 - greeks are here at the end. In a simple example where I solved for 50D beforehand, you can see how far from ATMF the 50D is when vol is high. The below was done with Julia.

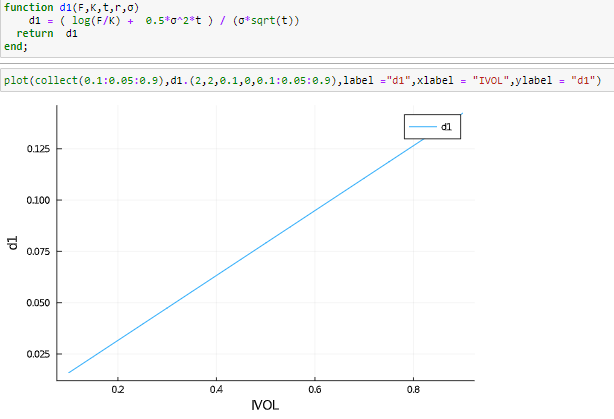

Generally, if $\delta = N(d1)$ excluding discounting, and $d1 =( log(F/K) + 0.5*σ^2*t ) / (σ*sqrt(t))$, you can see that for 100% moneyness, hence $F=K$, $d1>0$ which means it is above 50D which corresponds to N(0.0). It is an increasing function of vol:

-

1

-

1

-

1

$\begingroup$

$\endgroup$

For straddles ATM usually implies 0 delta. In general, ATM is determined by the market conventions in question.

$\begingroup$

$\endgroup$

2

When referring to a long straddle, atm means the 50 delta strike.