In Trading Volatility by Bennett, he says:

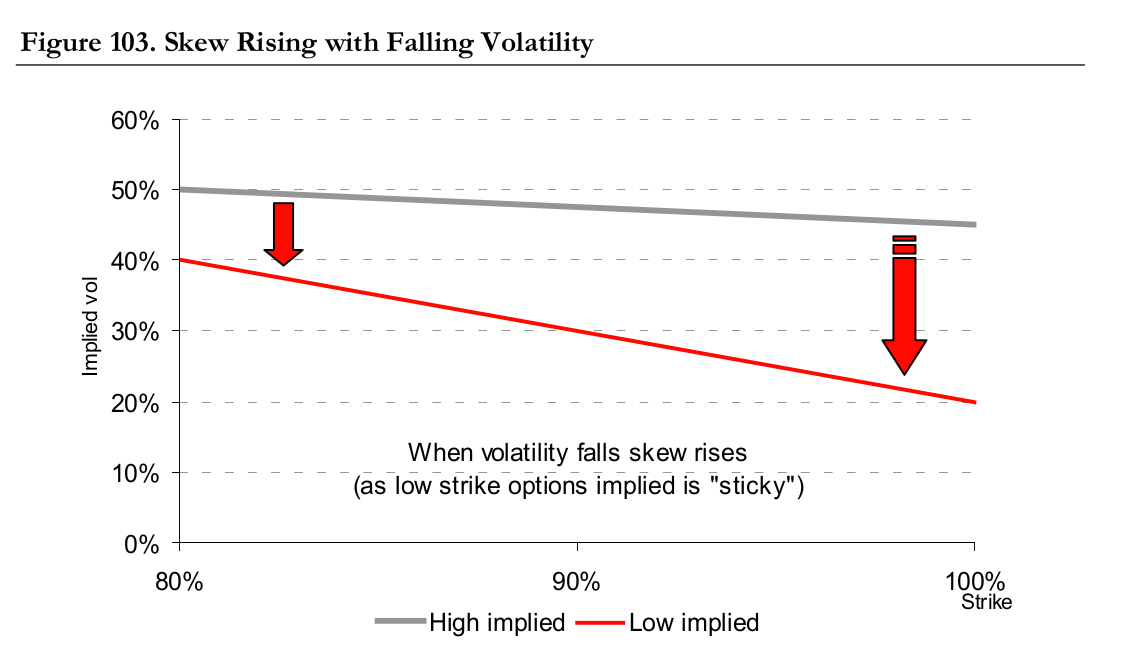

If there is a sudden decline in equity markets, it is reasonable to assume realised volatility will jump to a level in line with the peak of realised volatility. Therefore, low-strike, near-dated implieds should be relatively constant (as they should trade near the all-time highs of realised volatility). If a low-strike implied is constant, the difference between a low-strike implied and ATM implied increases as ATM implieds falls. This means near-dated skew should rise if near-dated ATM implieds decline (see Figure 103 above).

Doesn't this imply that there is a positive spot-skew correlation? When equities fall, we expect the low-strike implieds to remain relatively constant. However, ATM implied volatility usually goes up when equities fall. Therefore, the difference between low-strike implies and ATM implies will decrease as ATM implies rises (as it does when equities decline).