I'm trying to use the Black & Scholes to calculate the price for some options on the CBOE, but I'm having a hard time matching what I calculate with what i see on the market.

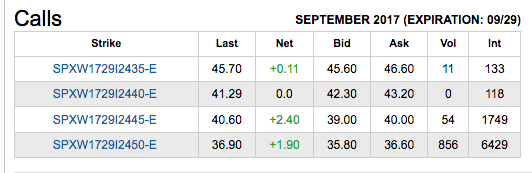

As an example I took the following screenshot (from this page):

At the time of writing, the numbers are as follows:

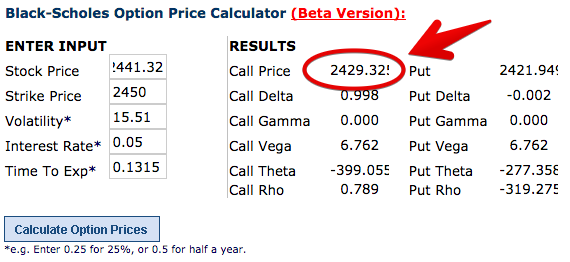

- S&P500: 2441.32

- VIX (from here): 15.51

Together with a risk free interest rate of 5% I calculated the price for the option with the strike price of $2450 using an online Black&Scholes calculator. The price I got for the call option is $2429.325:

$2429.325 is nowhere near the going rate of about $36 listed on the first screenshot above. Even if I multiply the rate of $36 with the usual multiplier of 100 I get $3600, which is also nowhere near the $2429.325 I got from the Black&Scholes.

Does anybody know what I'm doing wrong here? All tips are welcome!