Dividends are the key.

For simplicity, let's include a single dividend at the time of expiration, and assume that the options are European and expire ex. (There is really no reason not to assume that an option on a market index is European. EDIT: not quite true; that's discussed here.)

$S+P = e^{-rt}K+C + e^{-rt}D$

This is a certain fixed dividend, but that is not material to our purposes. Whether or not the dividend is subject to market risk and to what degree, or whether or not the dividend is correlated with a change in price of the underlying, it doesn't matter, because in any event, the present value of dividend(s), or what the market expects it to be, has absolutely nothing to do with the strike price of an option.

All is not lost:

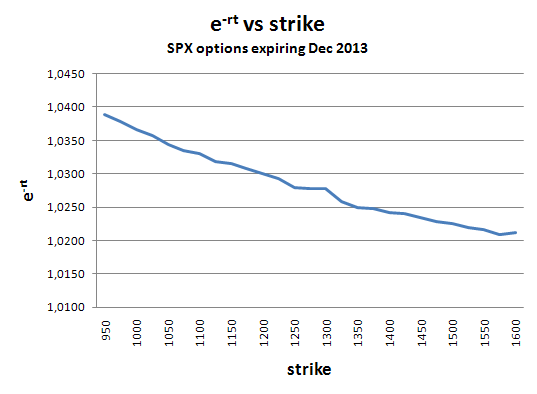

$e^{-rt} = \dfrac{S+P-C}{K+D}$

Take your spreadsheet, and solve for a fixed $D$ that makes that line flat. Then you will have $e^{-rt}<1$ as expected, and $e^{-rt}D$ is the present value the market places on underlying dividends from now to expiration.

EDIT #2 alternate way to work this out:

$S+P_1 = e^{-rt}K_1+C_1 + e^{-rt}D; \\ S+P_2 = e^{-rt}K_2+C_2 + e^{-rt}D.$

Subtract the first equation from the second:

$P_2-P_1 = e^{-rt}(K_2-K_1) + C_2 - C_1.$

Rearranging terms

$C_1-C_2+P_2-P_1 = e^{-rt}(K_2-K_1)$

we have created a synthetic bond from options at two different strikes which has an unambiguous interest rate because the value of any underlying dividends has cancelled out.