I am attempting to make a forecast of a stock's volatility some time into the future (say 90 days). It seems that GARCH is a traditionally used model for this.

I have implemented this below using Python's arch library. Everything I do is explained in the comments, the only thing that needs to be changed to run the code is to provide your own daily prices, rather than where I retrieve them from my own API.

import utils

import numpy as np

import pandas as pd

import arch

import matplotlib.pyplot as plt

ticker = 'AAPL' # Ticker to retrieve data for

forecast_horizon = 90 # Number of days to forecast

# Retrive prices from IEX API

prices = utils.dw.get(filename=ticker, source='iex', iex_range='5y')

df = prices[['date', 'close']]

df['daily_returns'] = np.log(df['close']).diff() # Daily log returns

df['monthly_std'] = df['daily_returns'].rolling(21).std() # Standard deviation across trading month

df['annual_vol'] = df['monthly_std'] * np.sqrt(252) # Annualize monthly standard devation

df = df.dropna().reset_index(drop=True)

# Convert decimal returns to %

returns = df['daily_returns'] * 100

# Fit GARCH model

am = arch.arch_model(returns[:-forecast_horizon])

res = am.fit(disp='off')

# Calculate fitted variance values from model parameters

# Convert variance to standard deviation (volatility)

# Revert previous multiplication by 100

fitted = 0.1 * np.sqrt(

res.params['omega'] +

res.params['alpha[1]'] *

res.resid**2 +

res.conditional_volatility**2 *

res.params['beta[1]']

)

# Make forecast

# Convert variance to standard deviation (volatility)

# Revert previous multiplication by 100

forecast = 0.1 * np.sqrt(res.forecast(horizon=forecast_horizon).variance.values[-1])

# Store actual, fitted, and forecasted results

vol = pd.DataFrame({

'actual': df['annual_vol'],

'model': np.append(fitted, forecast)

})

# Plot Actual vs Fitted/Forecasted

plt.plot(vol['actual'][:-forecast_horizon], label='Train')

plt.plot(vol['actual'][-forecast_horizon - 1:], label='Test')

plt.plot(vol['model'][:-forecast_horizon], label='Fitted')

plt.plot(vol['model'][-forecast_horizon - 1:], label='Forecast')

plt.legend()

plt.show()

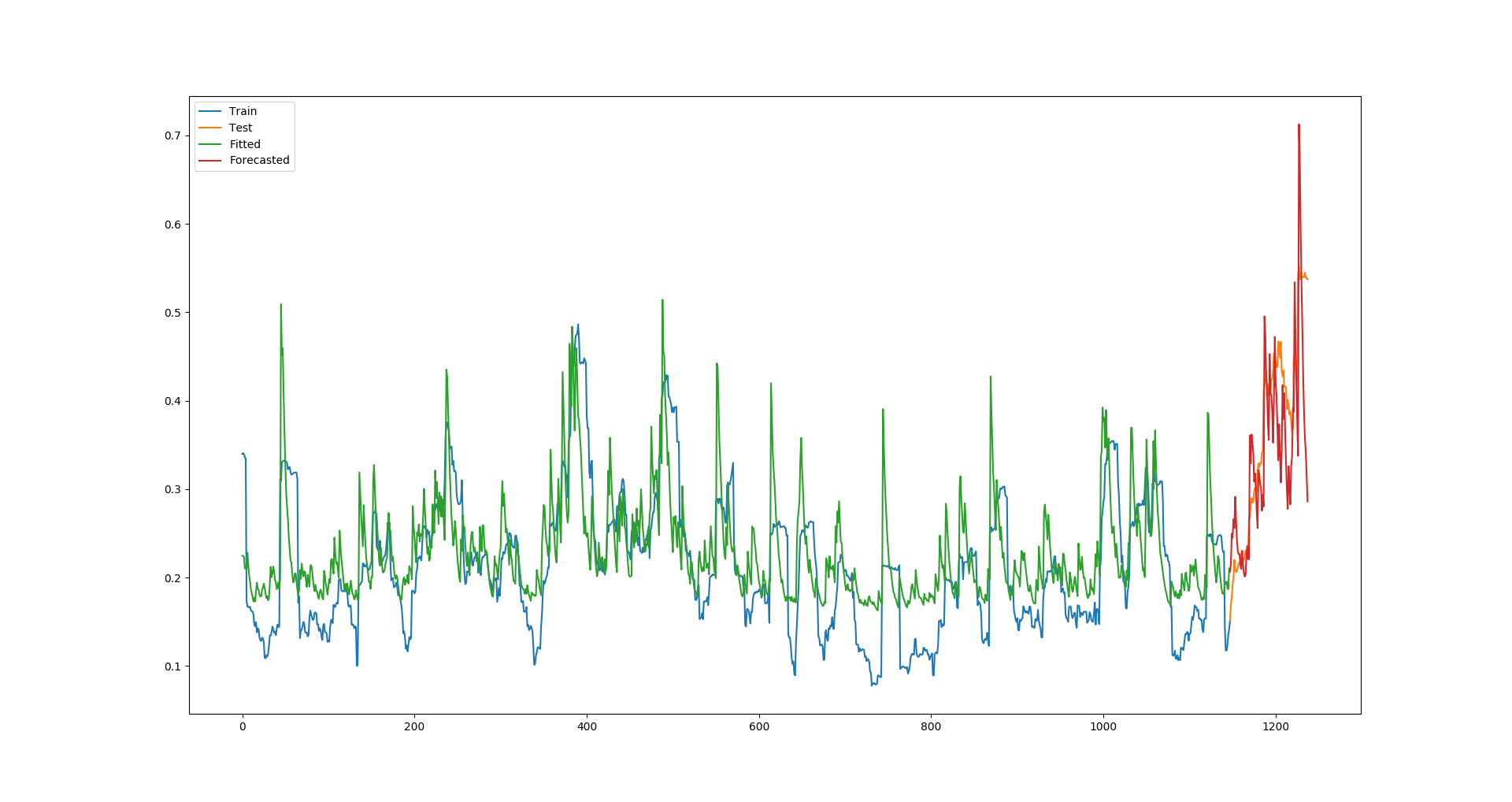

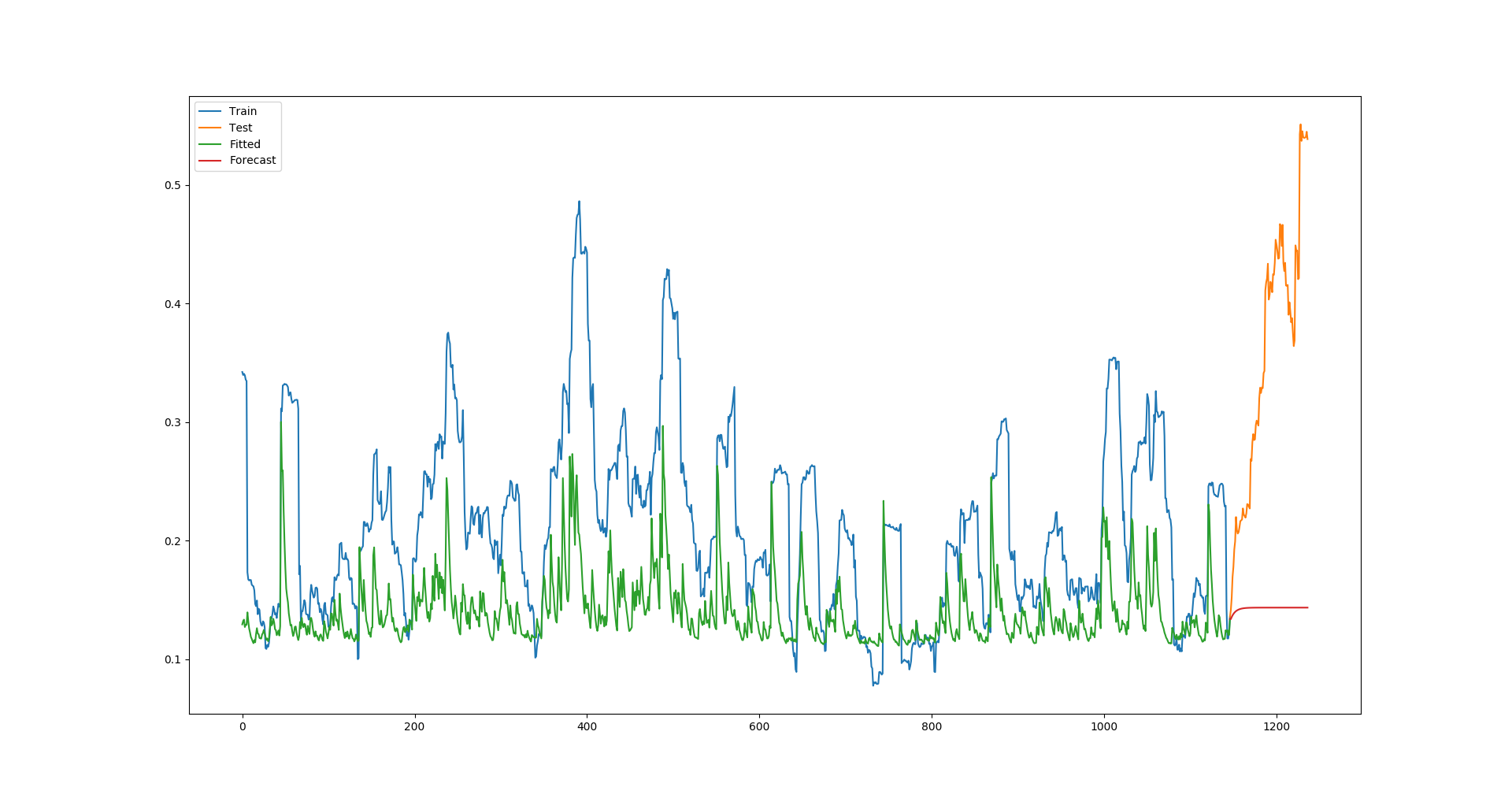

For Apple, this produces the following plot:

Clearly, the fitted values are constantly far lower than the actual values, and this results in the forecast being a huge underestimation, too (This is a poor example given that Apple's volatility was unusually high in this test period, but with all companies I try, the model is always underestimating the fitted values).

Am I doing everything correct, and the GARCH model just isn't very powerful, or modelling volatility is very difficult? Or is there some error I am making?