First time question, so please let me know if you have feedback for how I am asking.

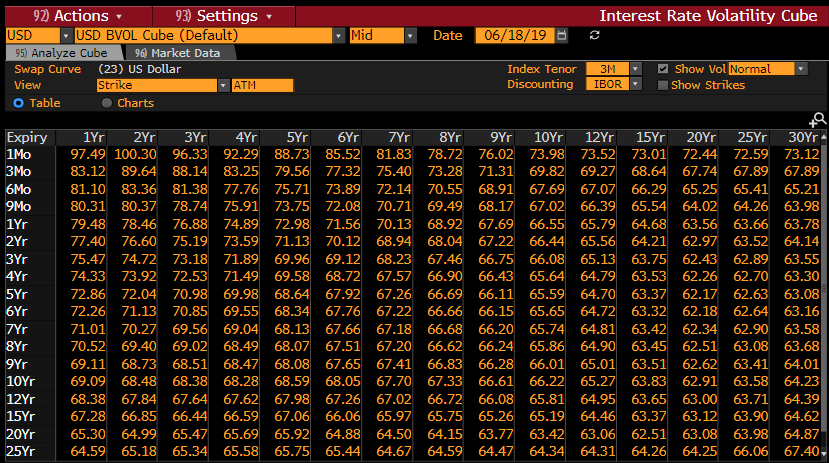

I am reading a market research piece and it makes reference to the performance of "vol, particularly the upper left and low strike receivers".

I've poked around looking for information on what that means. My understanding is that the volatility surface has x-axis of time to maturity, y-axis of implied vol, and z-axis of strike price. Should I infer that the 'upper left' vol would mean high implied vol with low time to maturity?

Thanks!