Here's a question that's been on my mind on-and-off for some time now.

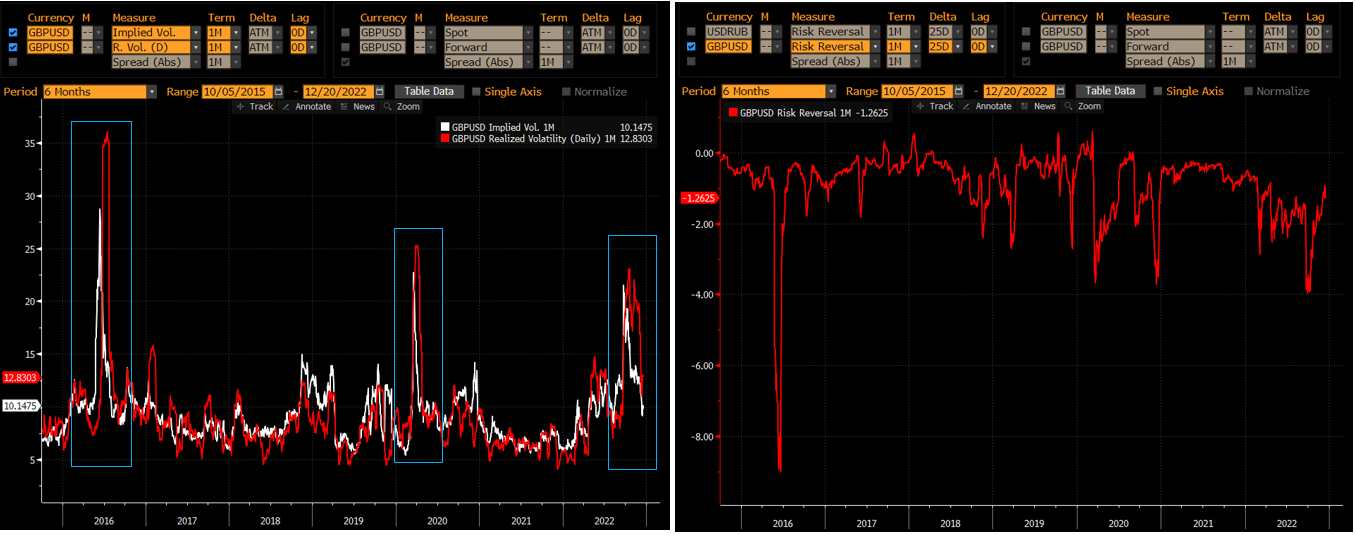

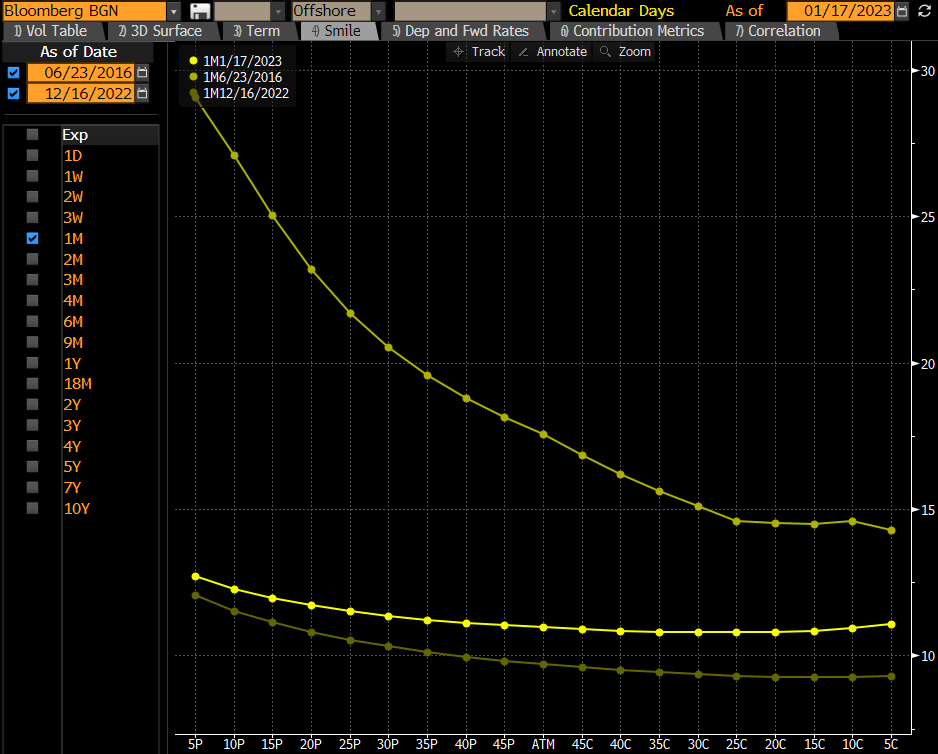

It's well known that Black-Scholes is an unsuitable model for pricing in the current (post 80s) market as it fails to capture the volatility smile/skew. A crude way around this is to calibrate a volatility surface by finding the volatility for which the market price agrees with the theoretical B-S price for a given set of strikes and maturities. Armed with this, we can price options which are consistent with the market. A better way is to use local or stochastic volatility models.

However, what I don't understand is that in each of these models, particularly B-S and local vol models, volatility is related to the underlying, not the option itself. As such, implied volatility seems to be making a statement about the forward-looking volatility, not of the option, but the underlying. In the Black-Scholes setting, we use a log-normal diffusion $$\mathrm{d}S_t = r_t S_t\mathrm{d}t + \sigma S_t \mathrm{d}W_t$$

and in a local volatility model we might amend this with a (deterministic) function $\sigma$ such that $$\mathrm{d}S_t = r_t S_t\mathrm{d}t + \sigma(t, S_t) S_t \mathrm{d}W_t$$

Now here comes my confusion. I can easily see how the time to expiry of an option might make a difference in the volatility the underlying exhibits over that time period. During a particularly turbulent time in the market we are perhaps expecting that the underlying might experience more volatility in the short term than in the long term, which could be reflected in option prices.

However I'm less convinced why the strike price should matter. Why should the strike price, which is inherently linked to the option, and the option alone, make any kind of statement about the volatility of the underlying? The closest intuition I can get is that the strike makes some sort of statement about the volatility of different regimes of the underlying price, such that we might expect something akin to

if the price of the underlying is to make it above strike $K_2$ it must pass through strike $K_1$ and the (expected) volatility in these regimes might differ

Any help with understanding this is much appreciated!