Note : We are considering the case of N risky assets.

I think the answer is 'Yes', although I am not sure as I am unable to prove it.

The reasons for me thinking that the answer is 'Yes' are -

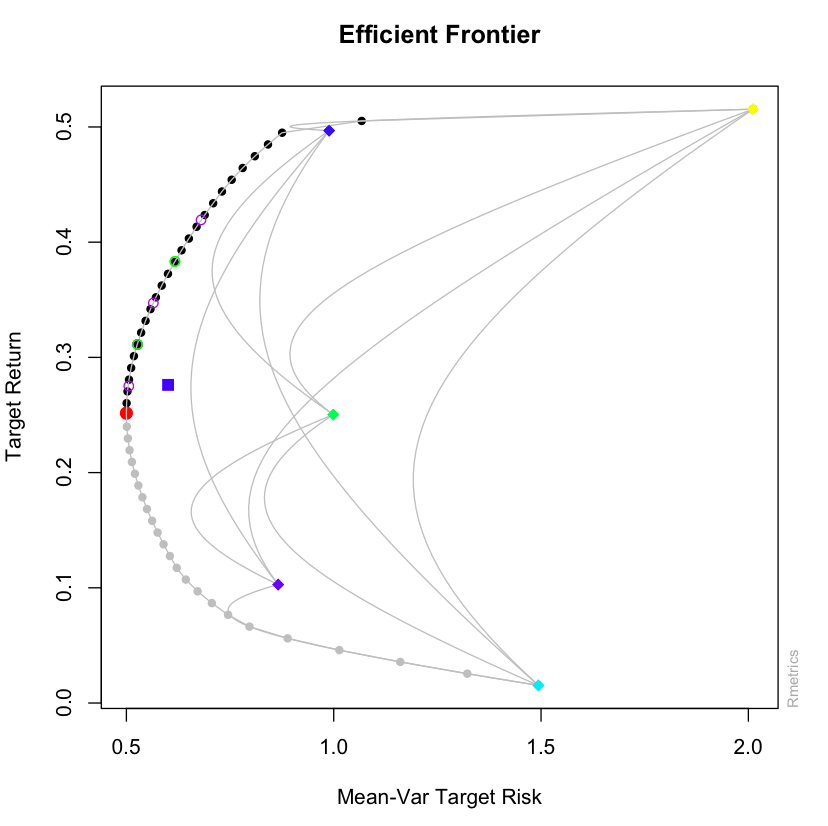

1) The two portfolios being considered are efficient, so they obviously lie on the efficient frontier.

2) We know that the linear combinations of any two portfolios form a parabola in the E-V space. So as a special case, the linear combinations of the two efficient portfolios being considered by us will also form a parabola in the E-V space.

3) The Efficient frontier for N risky assets is also a parabola in the E-V space.

4) So the only way the answer to my original question is 'No' is when the parabolas in (2) and (3) are not the same, which I think won't be possible geometrically.

(I think so because if the parabola in (2) is different than the one in (3), it will have to be below the one in (3), so that it stays in the efficient frontier, but at the same time pass through the two efficient portfolios being considered.)