You're right - I've looked, and there are many good tutorials on IR curve PCA out there, e.g. https://mockquant.blogspot.com/2010/12/principal-component-analysis-to-yield.html , https://plus.credit-suisse.com/r/kv66a7 , but I don't see anywhere a good explanation of atributing P&L to the IR curve changes in terms of PCs. Therefore I will outline it. Please ask if any details are unclear and suggest edits if you see errors.

We assume that:

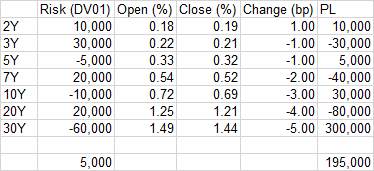

You use the same instruments on day 0 and day 1 to bootstrap the interest rate curve. The interest rate curve is defined by the levels of the instruments.

You know the change for each instrument from day 0 to day 1.

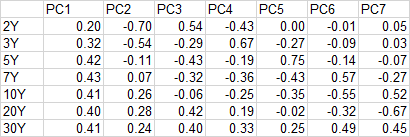

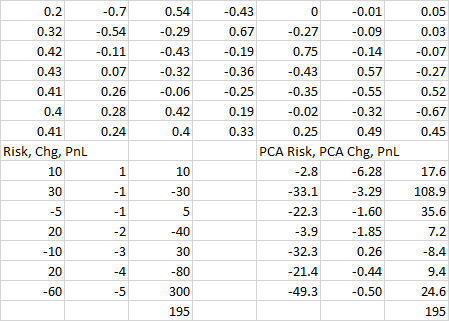

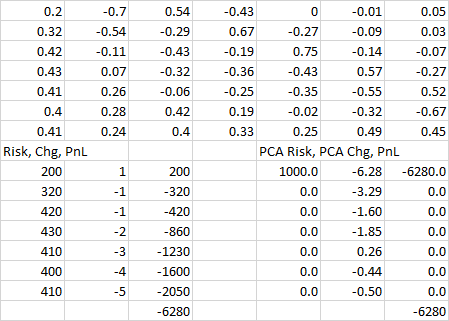

You know the loadings (the weight of each instrument) of the $p$ principal components, denoted $PC_1\ldots PC_p$.

However I don't want to assume that the interest rates sensitivities are strictly linear, i.e. that the dv01's tell us the whole story of the IR risk. Rather, we want the methodology to work even for highly non-linear instruments. You should fully reprice the portfolio using a perturbed interest rate curve if you can. However if you cannot fully reprice, and must estimate the P&L from the dv01's, let $\delta$ denote the vector of dv01's (P&L from small changes in each instrument, interest rate deltas).

Let $Y_0$ denote the interest rate curve on day 0, $M_0$ the mark to market on day 0, and $Y_f$ denote the interest rate curve on day 1.

In order to explain the P&L, we want to explain the change in the interest rate curve levels from $Y_0$ to $Y_1$ in terms of the PC's - each $PC_i$ moved by some $c_i$ that we will find.

For $i=1$ to $p$ - start loop on the principal components

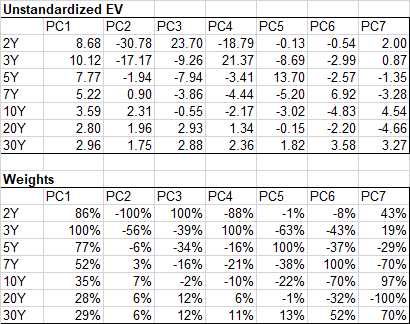

Solve for $c_i$, the change in the interest rates attributable to $PC_i$, that minimizes the distance between $Y_i \stackrel{\mathrm{def}}{=} Y_{i-1} + c_i PC_i$ and $Y_f$.

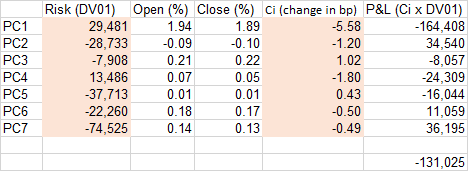

For better transparency, output $c_i$, and $c_i PC_i$ - the changes in the instruments explained by $PC_i$.

Estimate the P&L contribuion of each instrument by multiplying $\delta$ and $c_i PC_i$. Report these P&L estimates and their sum (the P&L from $PC_i$ move estimates from dv01's).

If you can fully reprice the profolio: let $M_i$ denote the mark to market using curve $Y_i$. Report $M_i - M_{i-1}$ as the more accurate P&L attributable to the $c_i$ change in $PC_i$.

For a more complete picture, if $i>1$, then let $y'_i$ denote $y_0 + c_i PC_i$ - the interest curve obtained by perturbing only $PC_i$ and no other PCs. Reprice the profolio: let $M'_i$ denote the mark to market using curve $Y'_i$. Report $M'_i - M_0$ as the P&L attributable to the $c_i$ change in $PC_i$ and no other PCs.

Otherwise if you don't want to fully reprice, then just use the P&L estimated from the dv01's.

Next $i$ - end loop on the principal components

Report residual P&L not explained by this methodology.