Target redemption forwards (TARFs) are a widely used instrument in the FX market, but their variations often make their payoffs complex and not easily understood.

Key Concept:

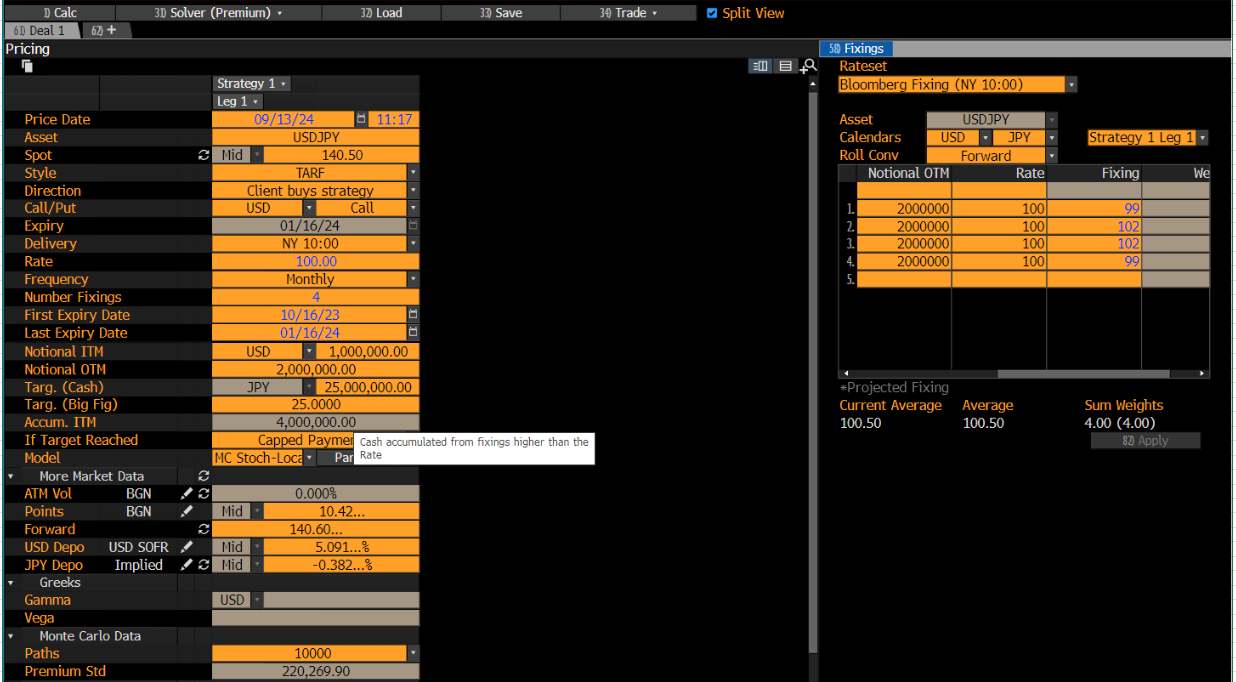

In the most common TARFs, only positive payoffs contribute towards reaching the target. This can be seen in the Bloomberg screenshot, where I manually entered fixings and a strike rate for simple mental calculation. The tooltip for the field labeled Accum. ITM highlights that only Cash accumulated from fixings higher than the Rate counts. The field name itself implies that only in-the-money (ITM) positions are considered. In this case, the accumulated profit of 4 million arises from the two instances where the fixing is 102 and the strike is 100, with 1 million notional value.

If you have access to Bloomberg (with an anywhere license / own fingerprint login), you can access DLIB. It is a great (educational) tool for structured products in general, particularly the BLAN templates, because these show the code for the payoffs. As you can see below, it only accumulates if the value is positive (hence ITM).

let tarf (acc, (obs, pay)) =

let previous_amount_accum, target_counter, all_flows = acc in

let spot_fixing = fix(obs, ccy_pair) in

let cond_option = if is_call then spot_fixing - strike else strike - spot_fixing in

let this_accumulation = max(cond_option, 0) in

let new_amount_accum = previous_amount_accum + this_accumulation in

General Description from a Term Sheet:

A typical term sheet might describe the knockout event like this:

The Knockout event is triggered when the cumulative in-the-money (ITM)

value of the current and previous strips equals the target profit. The

ITM value is the difference between the prevailing FX rate and the

strike, floored at zero. Once the target is reached, future

settlements are canceled, the gains are locked, and you are no longer

hedged.

Common Payoff Variations After Target is Hit:

- None: No payment is made for the final period.

- Capped: Payments are limited to a pre-determined cap (most common).

- Full: All positive gains are realized.

A Broader Understanding of TARFs:

A TARF in general is a lot more than that. I do not think it has been asked frequently here, but TARF payoffs are definitely a common source of confusion with new employees / traders at the places I worked at. Therefore, I think a more detailed explanation might help some.

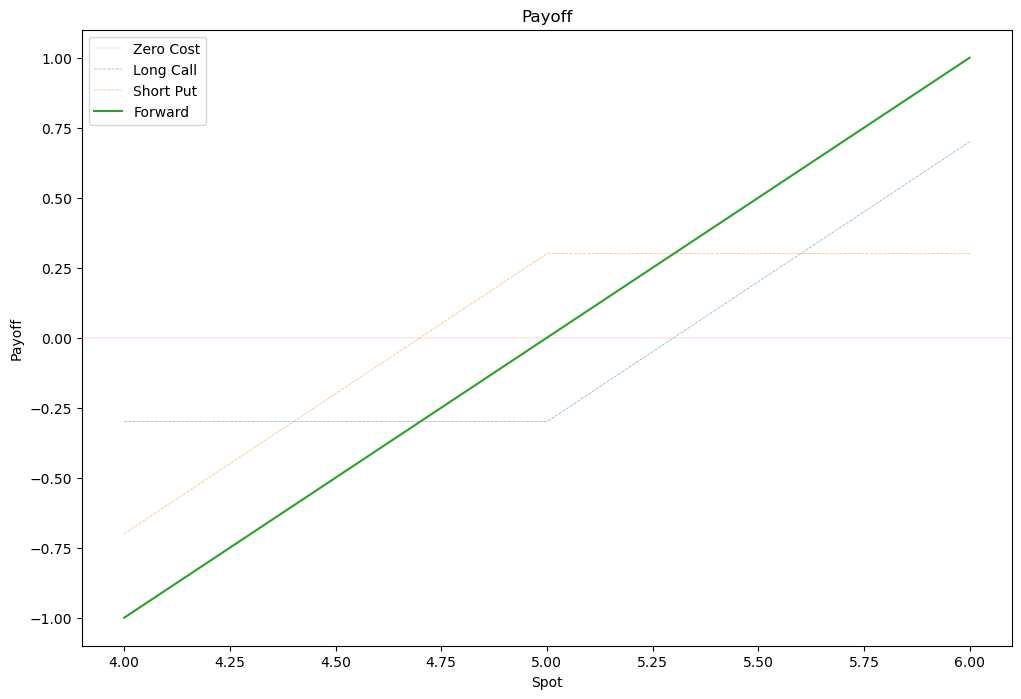

Fundamentally, a forward contract can be replicated with put and call options, as shown in the chart below. More details are available in this answer.

The core idea of a TARF is to provide a "better" forward rate (strike). To achieve this, the downside is usually leveraged (higher notional).

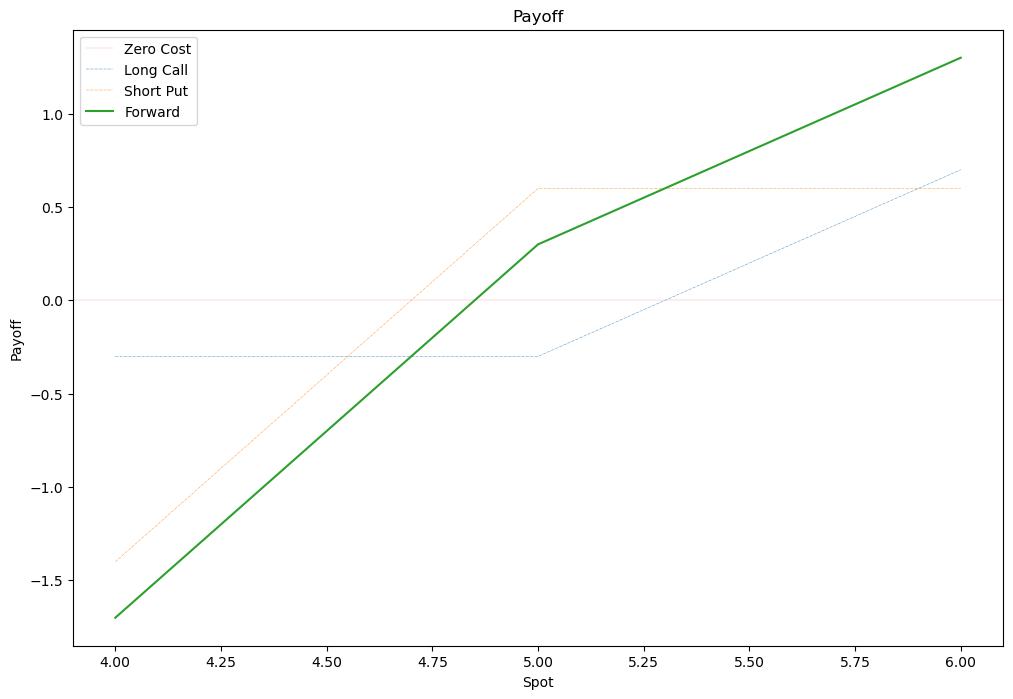

So far, this was only a one period consideration. A TARF is really a strip of options which ceases to exist (knock out) once a cumulative Target profit is

reached. This target caps the upside. If you keep the "unlimited" leveraged downside, you get even cheaper product (more "favourable" strike).

Knock-in TARF

That leveraged downside is obviously a big risk not everyone is willing to take (some are not fully aware of it to be honest). Therefore, it is common to place an EKI (European Knock-in), meaning the OTM leverage side has to knock-in before it is "live. If the product has not reached the accumulation cap at the fixing:

- If fixing > rate, then the buyer of the TARF buys the ITM notional at the rate.

- If barrier < fixing < rate, there is not settlement.

- If fixing < barrier, then the buyer of the TARF buys the OTM notional at the rate

Dual Strike Tarf

Instead of a EKI, you can have separate ITM and OTM strikes.

If the product has not reached the accumulation cap at the fixing:

- If fixing > upper rate, then the buyer of the TARF buys the ITM notional at the upper rate.

- If lower rate < fixing < upper rate, then there is no settlement.

- If fixing < lower rate, then rthe buyer of the TARF buys the OTM notional at the lower rate

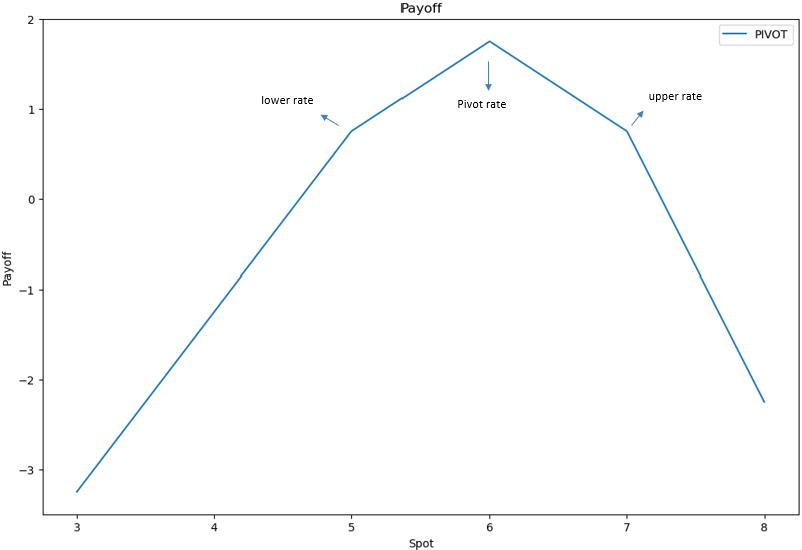

PIVOT Tarf:

A Pivot TARF acts like a standard TARF unless the pivot rate is breached. After this, the structure reverses. Therefore, there are three levels for this structure: lower rate, pivot rate, and upper rate (in ascending order).

If the product has not reached the accumulation cap at the fixing:

- If fixing < lower rate, then the buyer of the TARF buys the OTM notional at the lower rate.

- If lower rate < fixing < pivot rate, then the buyer of the TARF buys the ITM notional at the lower rate.

- If pivot rate < fixing < upper rate, then the buyer of the TARF sells the ITM notional at the upper rate.

- If fixing > upper rate, then the buyer of the TARF sells the OTM notional at the upper rate.

In a chart (somewhat sloppy, due to time constraints), this looks like as follows:

Looking at the DLIB Template, you can see that it is indeed 4 legs put together, and plenty of choices on top of the ones mentioned so far.

In essence, the PIVOT TARF accumulates towards the target when spot is between the upper and lower level: these gains, relative to the pivot rate, are cumulative towards "Targ. (Cash)." or Targ. (Big Fig). The latter is something that confuses most people who are not working with FX frequently. In the OVML example with USDJPY from above, you can see that 25 Mio JPY in Cash are just 25 Big fig. The DLIB deal is using a EURUSD with settlement in Cash DOM. The deal manually was set to reach the target immediately.

That is why the pricing engine states the Model is Deterministic (it was already hit and all payoffs are known). The Call strike is 0.8 and the fixing was set (manually) to 1, which means we breached the 0.1 target (1-0.8 = 0.2). We get a capped payment, meaning 0.1*ITM Notional = 40000. However, in USD that is 40000/K = 50.000, which is what is displayed in the Cashflows section of DLIB.

Variations of the (PIVOT) TARF:

As can be seen in the DLIB Template, there are lots of possible variations.

The regular barriers in the customized Payoff section are creating the PIVOT TARF payoff. You can set separate strikes for each leg, separate barriers (Up & Out, Down & Out, Up & In, Down & In), continuous vs discrete barriers, global barriers, barrier rebates, use several possible targets (Big figure, cash, counter etc), include the other leg(s) in the ITM (or OTM) target, collars, ...

Exotic TARFs

Since TARFs are not exotic enough (it seems), you can trade numerous types. Some are for example:

- Individual KO (one / several legs remain active if one / several others KO)

- Callable and Putable TARFs

- Range Target TARFs: If outside a range, you will face a penalty strike, bonus strike, or some other additional payoff feature.

- Forward Start TARFs: Strikes will be fixed on future dates depending on the prevailing spot rates at some future time.

- Dual (Triple) currency (Pivot) Chooser TARFs: For example, on each settlement date, if EURUSD performance < GBPUSD performance, client sells EURUSD at EURUSD strike, else client buys GBPUSD at GBPUSD strike where performance is frequently defined as

(EURUSD Strike - EURUSD Spot Fix)/EURUSD strike or GBPUSD Spot - GBPUSD Strike)/GBPUSD Strike.

- Conditional TARFs: It could be called a Knock-In TARF it it would not exist under a different name already. You will have two targets. The first will KI your actual TARF (if reached), after which you have a normal TARF payoff. There can also be forced KI dates, if not KI at a certain date already.

....

Side remark with regards to pricing. LV will not be a useful model for these type of options. As long as its a single underlying SLV should be fine, provided it is calibrated to barrier options. Once you try to price Chooser TARFs you will get quickly into the realm of a good tweet I stumbled upon some time ago. Many people tend to think if a tool gives a price it works (here Monte Carlo Local Vol). However, that is classic GIGO.

TARFs and Autocallables are so popular because they seem to offer great deals. However, there is no such thing as free money and the better it seems, the worse the potential downside will be.

Disclaimer:

Parts of the definitions are taken from the help page of Bloomberg DLIB and OVML.